Mortgage debt is the third area of money creation that we examine for associations with inflation. Two previous studies have analyzed the areas of federal government deficit spending1 and consumer credit.2

From Photo by Kindel Media from Pixabay

Introduction

In this project, we examine the correlation between changes in mortgage debt and changes in inflation as measured by the Consumer Price Index (CPI3). The Federal Reserve data for Mortgage Debt Outstanding, All holders (1949-2019)4 is the mortgage data for this study.

The hypothesis we are testing is that inflation depends on mortgage debt in a linear manner, expressed in the following equation:

I = mS + b

where

I = Change in CPI (the Consumer Price Index)

S = Change in Mortgage Debt

The two constants, m and b, define the relationship of y, the dependent variable, to x, the independent variable. By writing the relationship in this way, we imply that CPI (y) depends on mortgage debt(x). But this is a mere formality because the equation can be rearranged:

S = m’ I + b’

where

m’ = 1/m

b’ = -b/m

We could just as well write the equivalent equation implying that mortgage debt depends on inflation without affecting results and conclusions.

Data

The data is organized similarly to the federal deficit spending and consumer inflation study.5 The inflation time series is divided into periods of inflationary surges, deflationary surges, and years when inflation/disinflation/deflation have trends with <4% change uninterrupted by countertrend moves >1.5%. The three types of inflationary periods from 1952-2022 are in Table 1. For the definition of the various periods, see “Consumer Credit and Inflation. Part 4”.2

Table 1. Timeline of Inflation Data 1952-2022

The quarterly data displays more information than the yearly data used previously.6

- Table 4 has 8 periods with positive inflation surges for the 70-year period. The previous study defined only 5.

- There are 5 negative inflation surges in Table 4, one more than in the previous study.

- There are also 5 time periods with insignificant inflation changes in Table 4, while the previous study had only 3.

- Significant inflationary periods are identified here for 2006-08 and 2009-11 with the quarterly data. A significant deflationary period was identified for 2008-09.

- There were 3 1/2 years 1983-86 with no significant inflation changes that were not identified previously.

Note: 1999-2020 had been identified previously as a 22-year period with no significant inflationary trends. The quarterly data found two significant inflationary trends and one significant deflationary trend within the interval.

Using the quarterly data gives an apparently better resolution of inflationary and deflationary periods than was obtained with the annualized data. Whether or not this is useful remains to be seen with further analysis.

Comparing Mortgage Debt Growth to Inflation

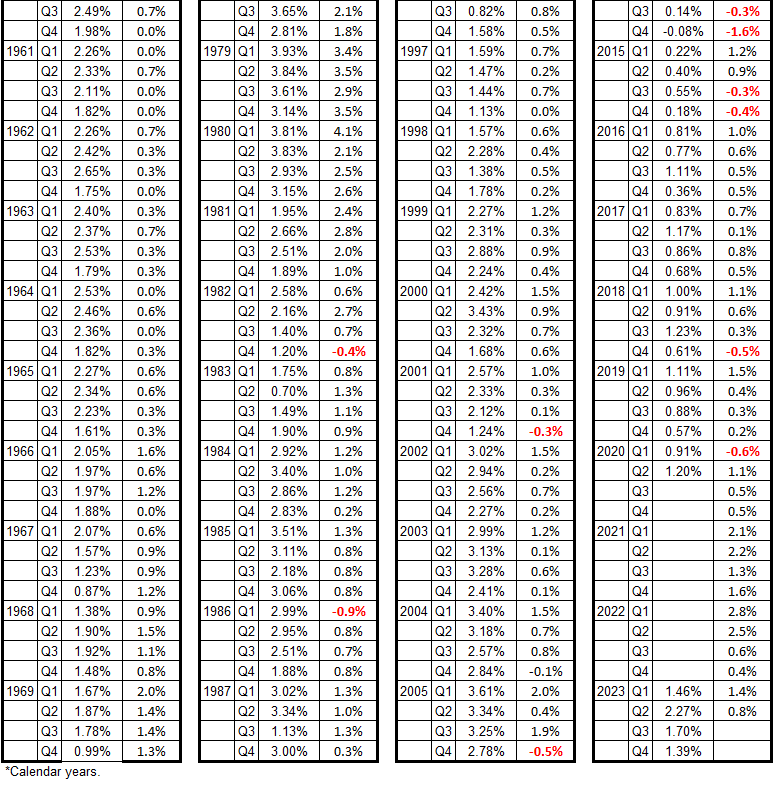

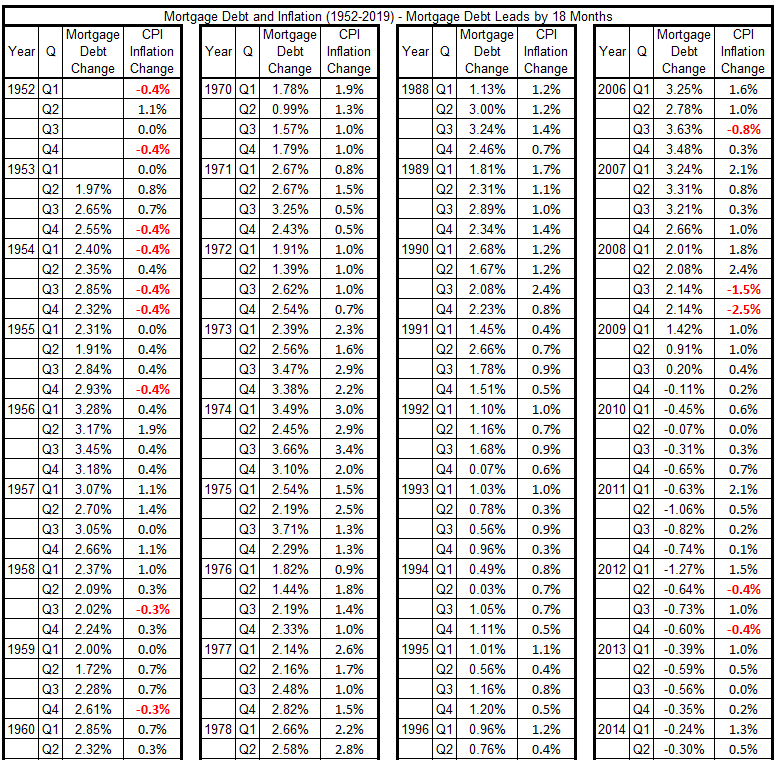

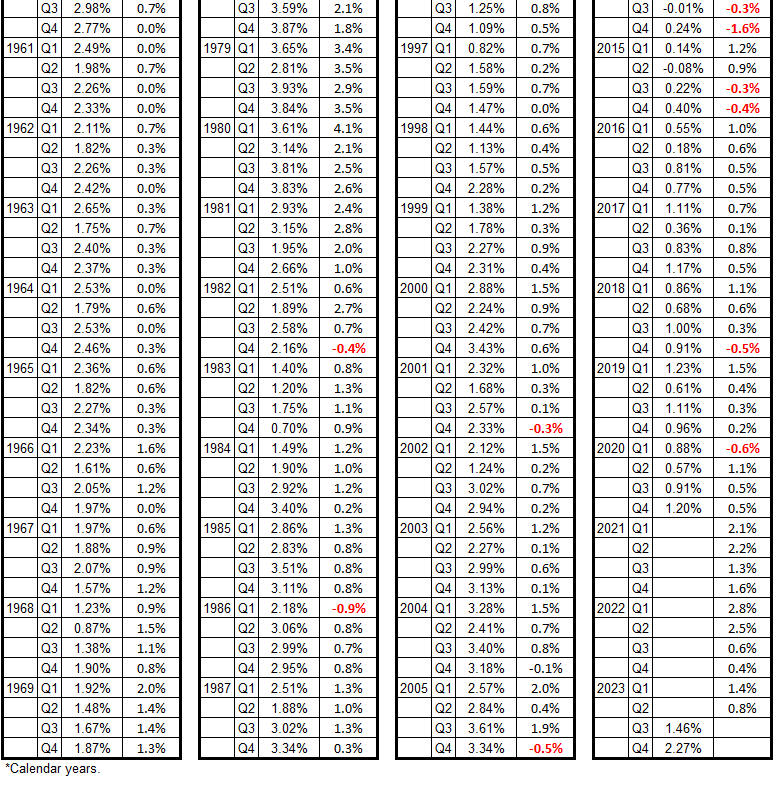

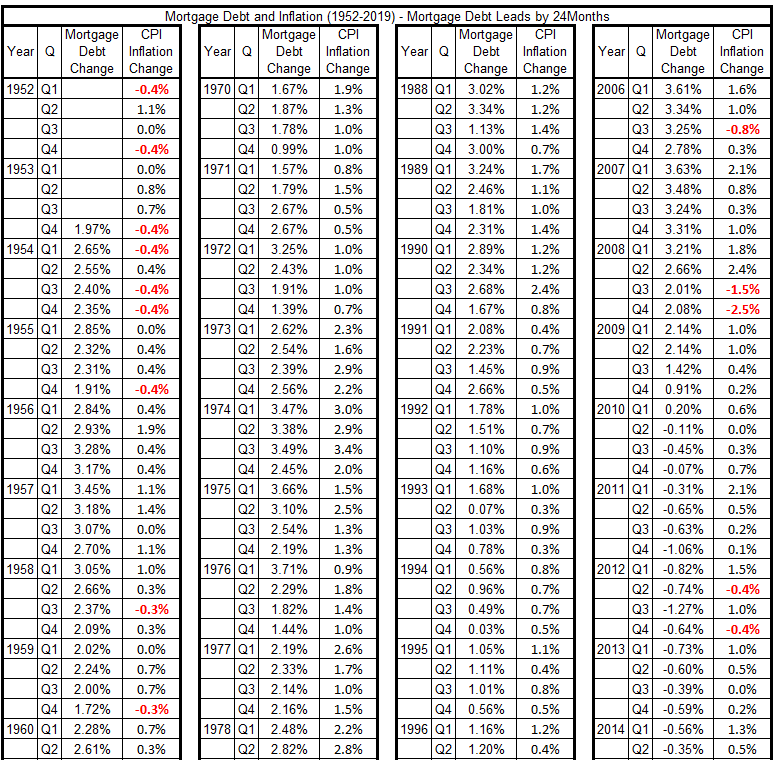

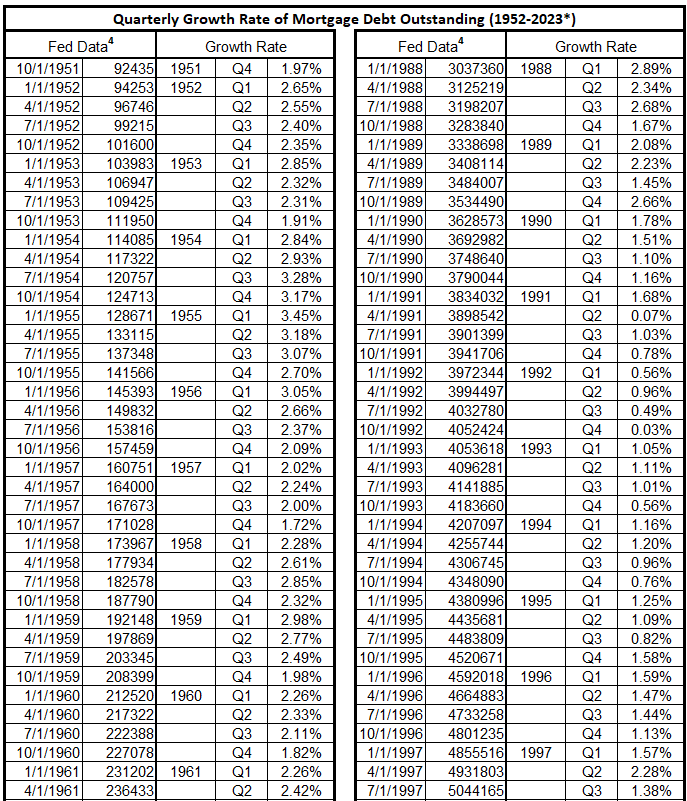

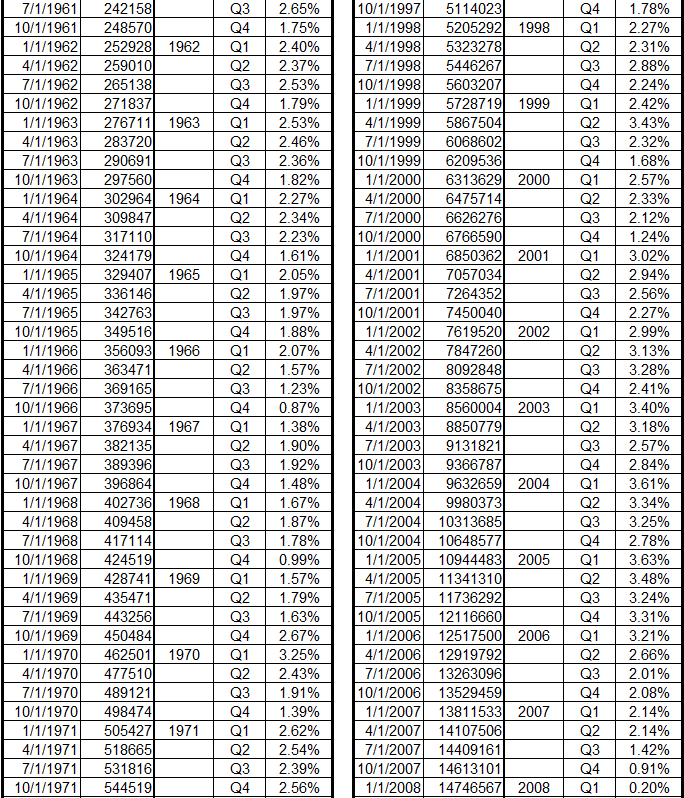

The determination of the mortgage growth rate by calendar year quarters is shown in Appendix 1. Tables for comparing mortgage debt with inflation are constructed below from that growth rate data.

We use the Consumer Price Index (CPI) to calculate the inflation rate, as was done in the previous study of federal deficit spending.5 However, the data here for inflation growth is organized by calendar year quarters, as shown in Appendix 2.

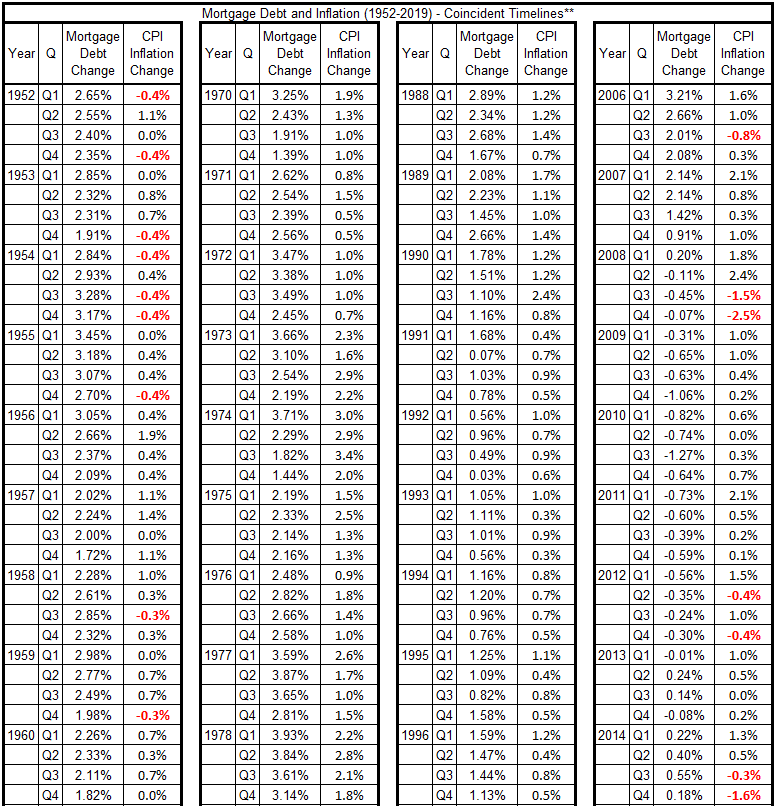

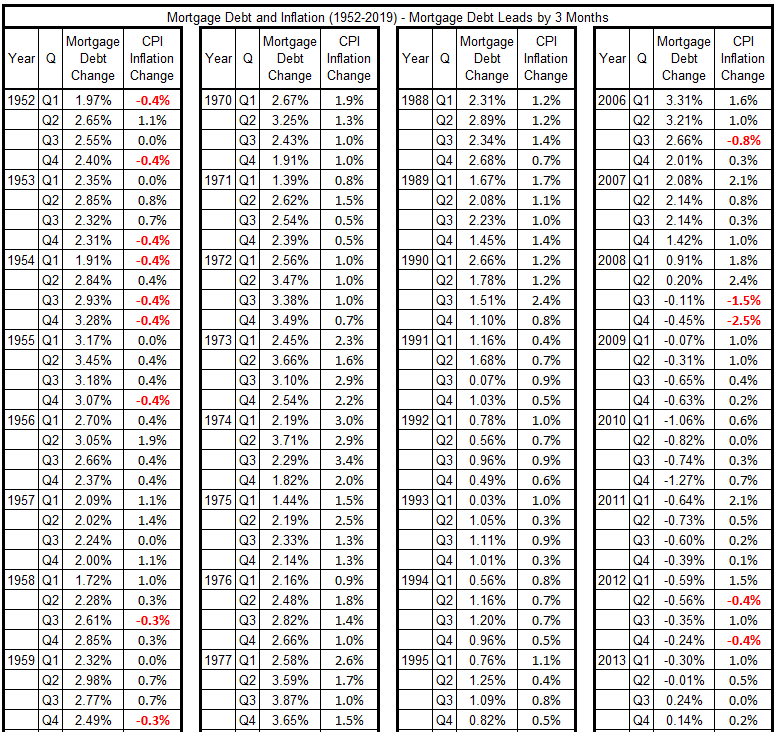

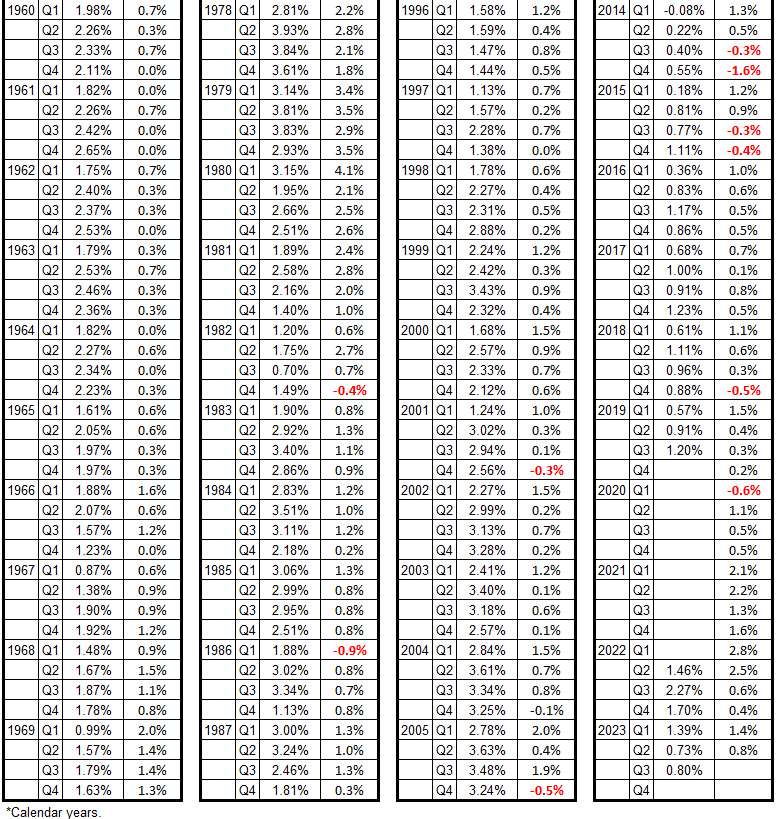

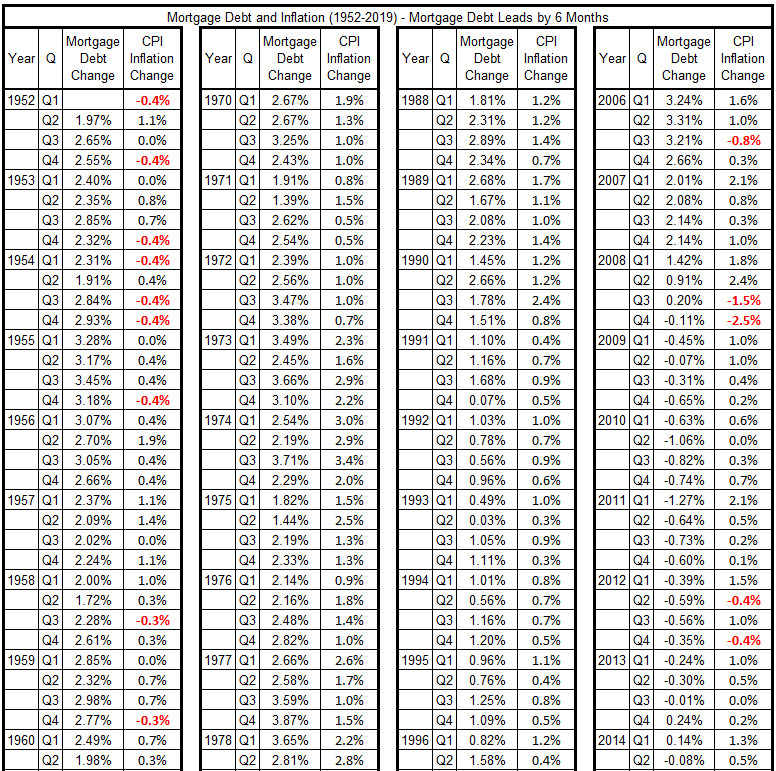

The thirteen tables below show coincident timelines for the two variables (Table 2) and then timeline offsets by +/- 3 months, +/- 6 months, +/- 9 months, +/- 12 months, +/- 18 months, and +/- 24 months. Tables 3 – 8 give the data for mortgage debt growth leading CPI growth. Tables 9 – 14 have the data for CPI growth leading mortgage debt growth.

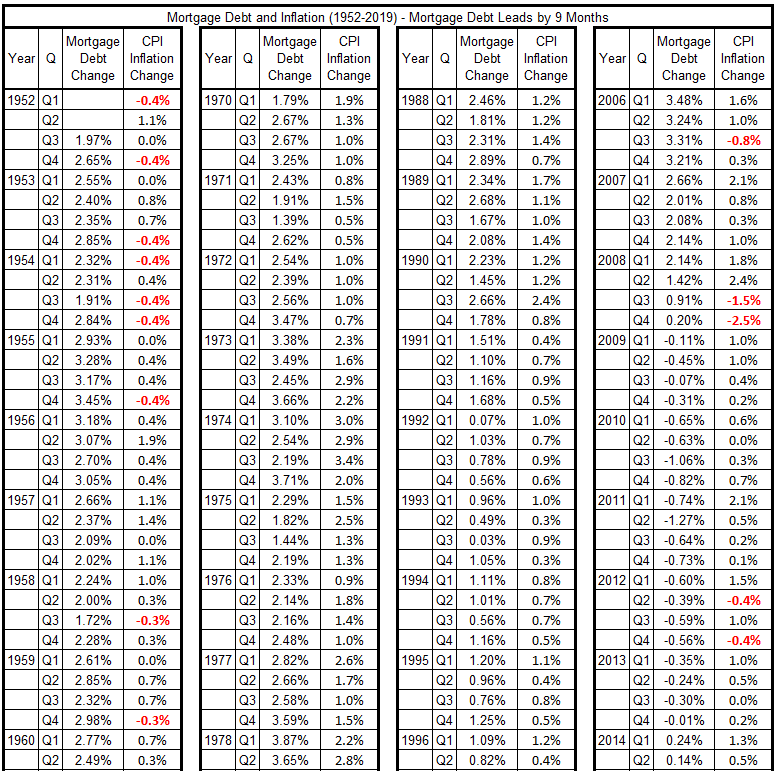

Table 2. Mortgage Debt Growth and Inflation (CPI), Coincident Data, 1952-2019*

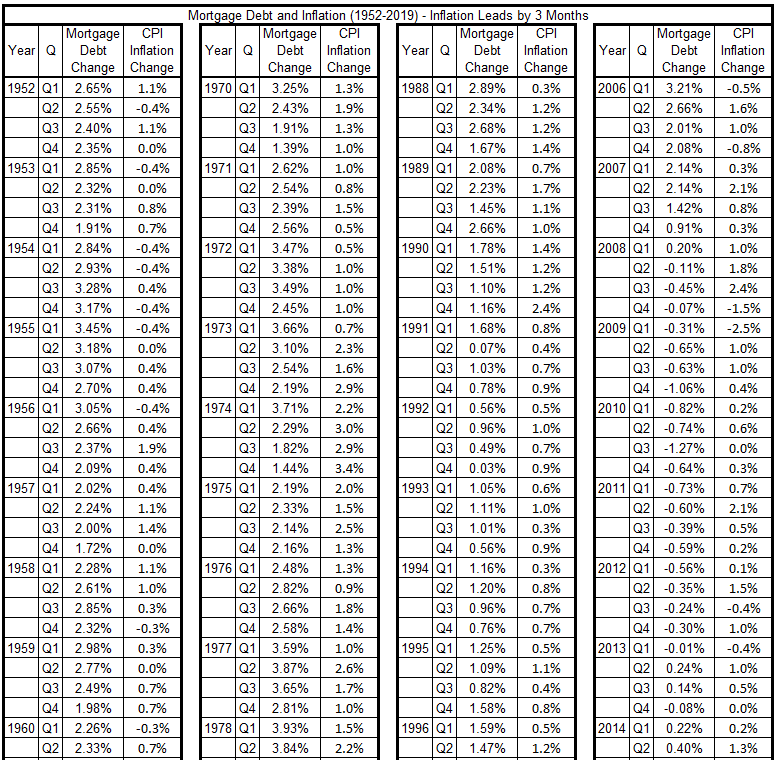

Table 3. Mortgage Debt Growth and Inflation (CPI), Mortgage Leads by 3 Months, 1952-2019*

Table 4. Mortgage Debt Growth and Inflation (CPI), Mortgage Leads by 6 Months, 1952-2019*

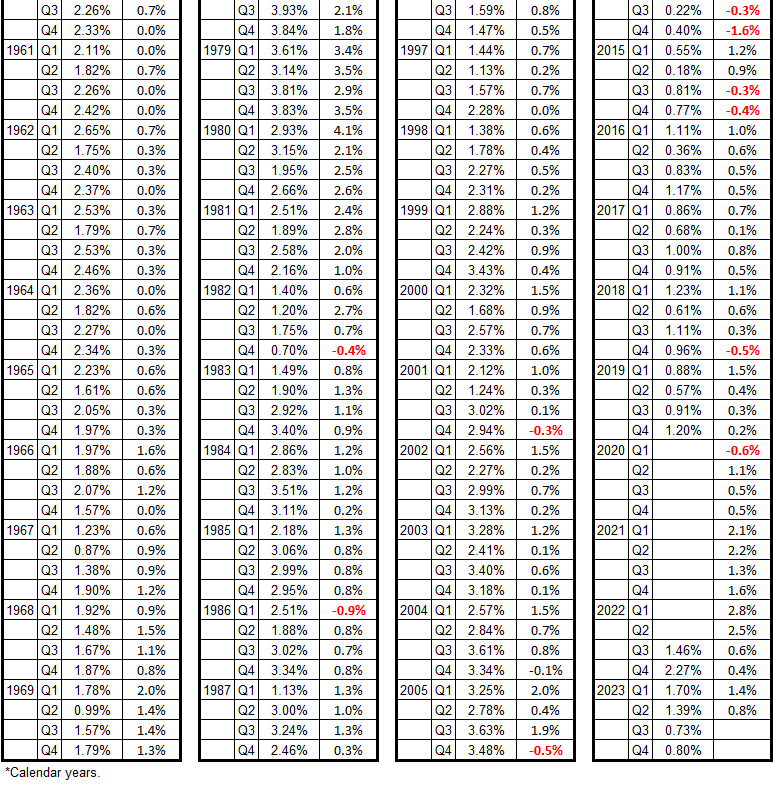

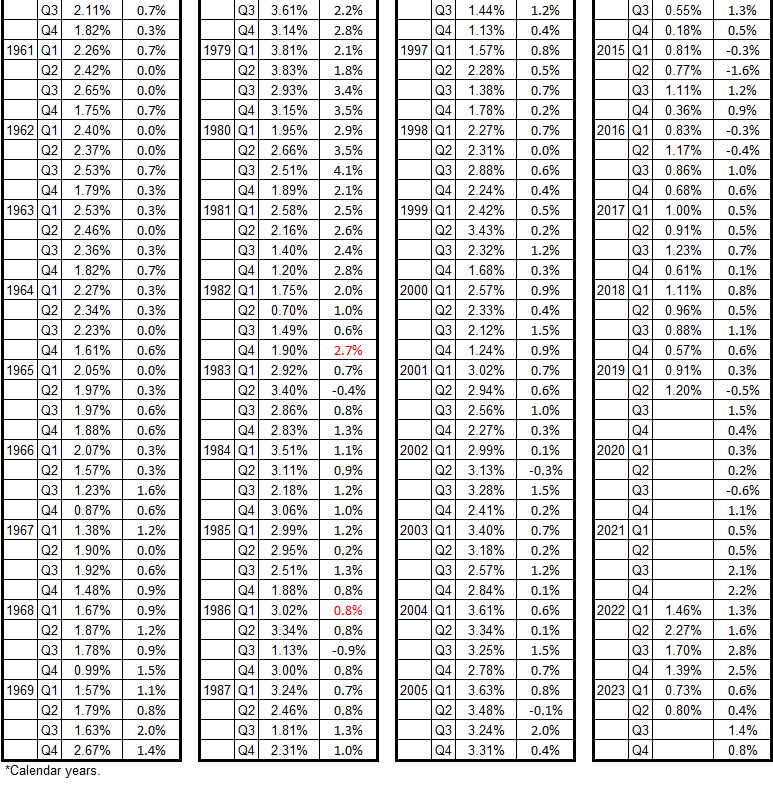

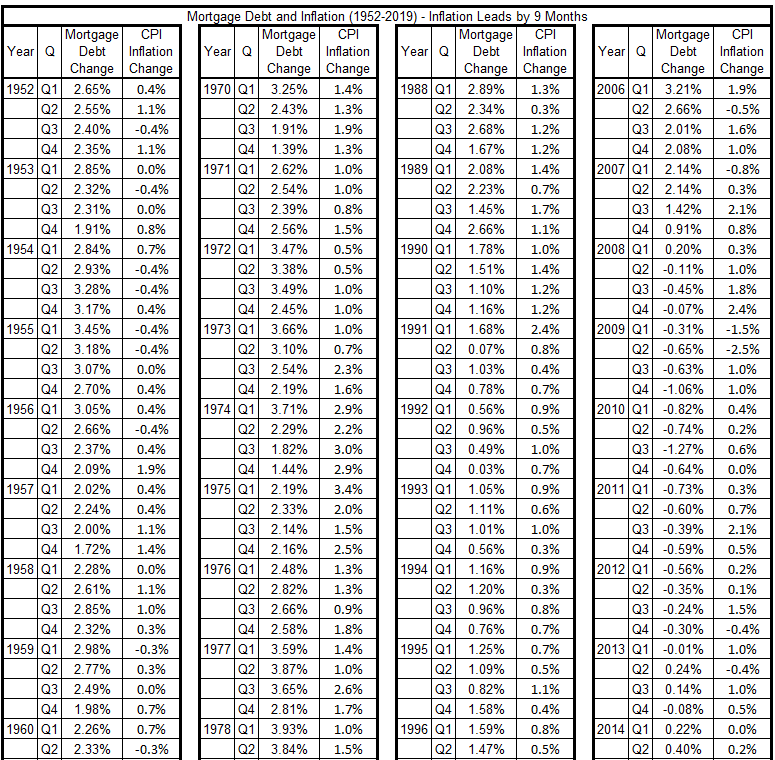

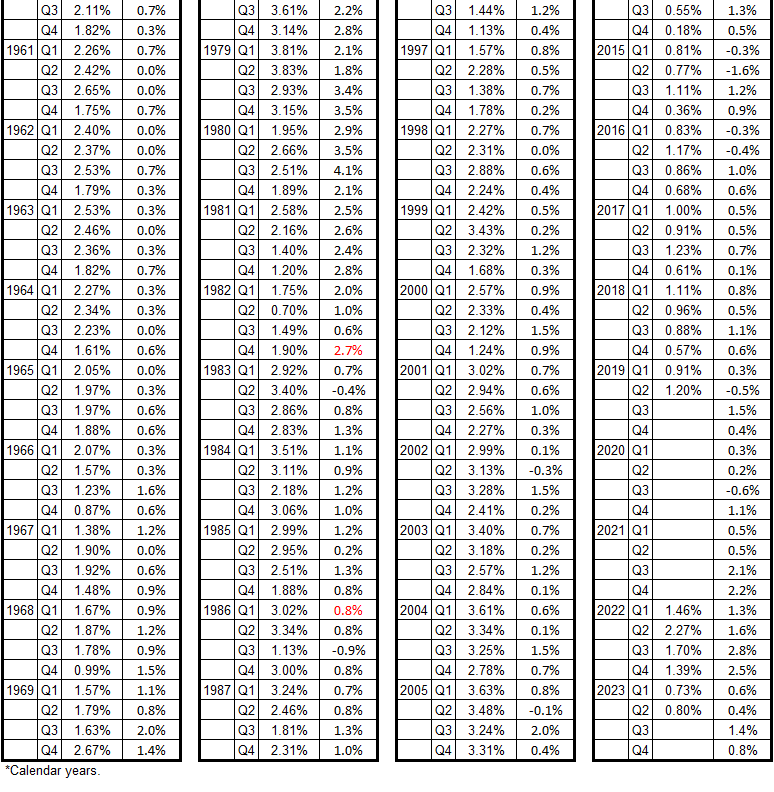

Table 5. Mortgage Debt Growth and Inflation (CPI), Mortgage Leads by 9 Months, 1952-2019*

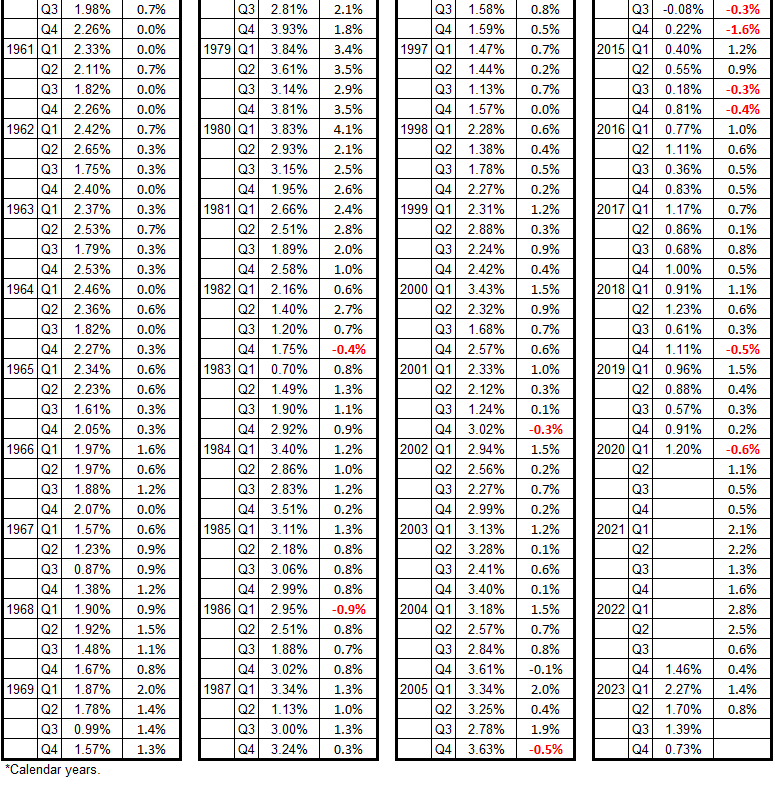

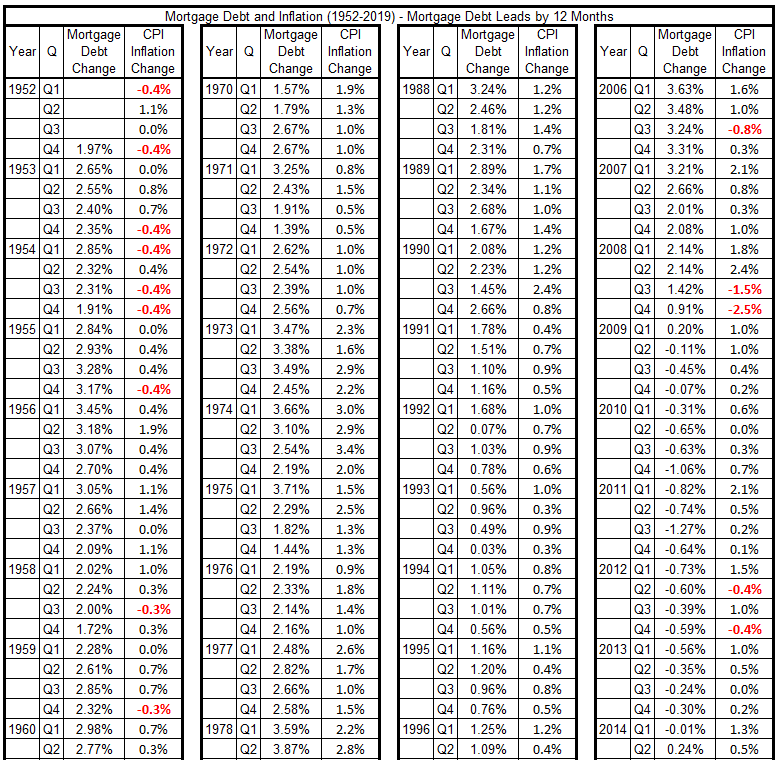

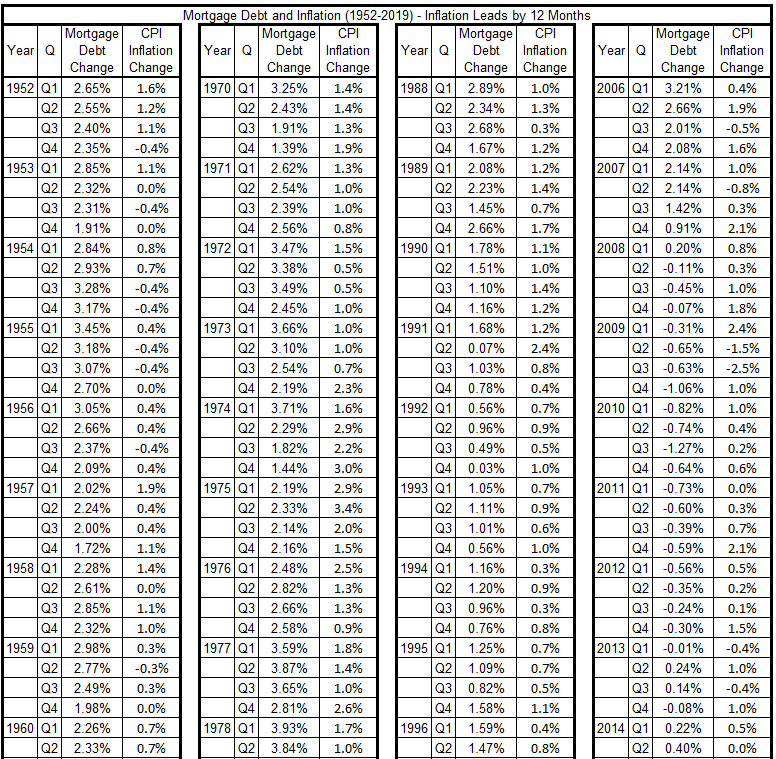

Table 6. Mortgage Debt Growth and Inflation (CPI), Mortgage Leads by 12 Months, 1952-2019*

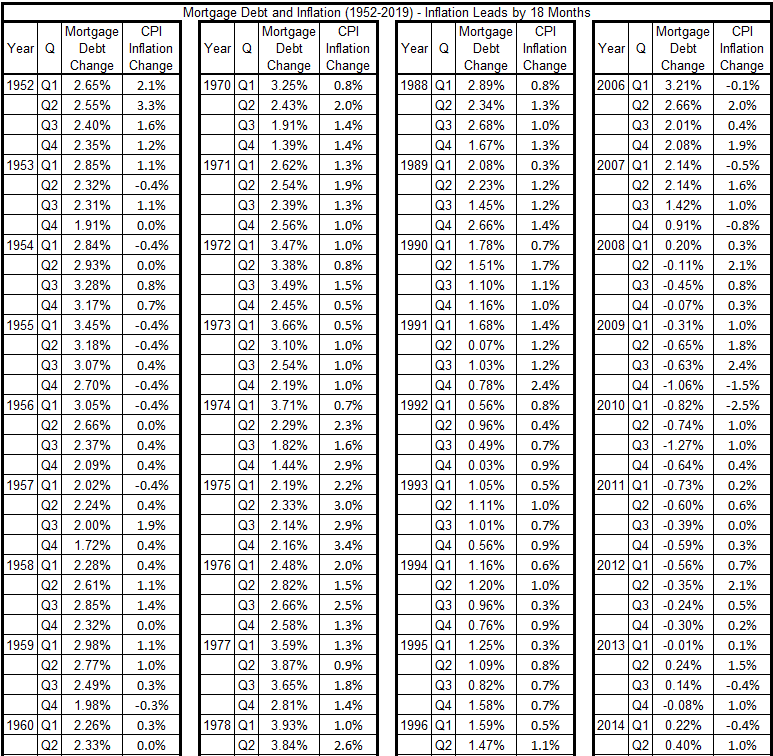

Table 7. Mortgage Debt Growth and Inflation (CPI), Mortgage Leads by 18 Months, 1952-2019*

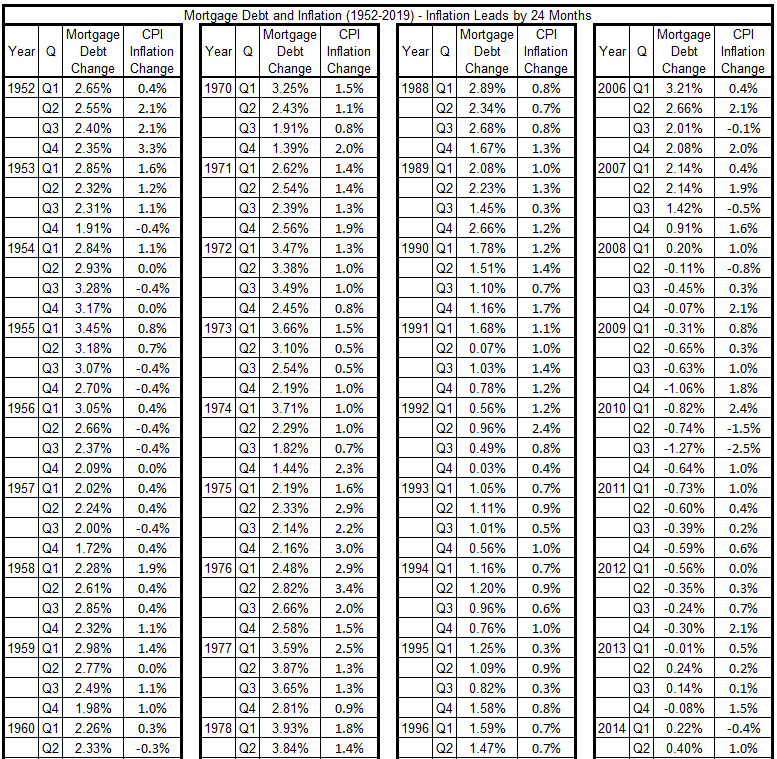

Table 8. Mortgage Debt Growth and Inflation (CPI), Mortgage Leads by 24 Months, 1952-2019*

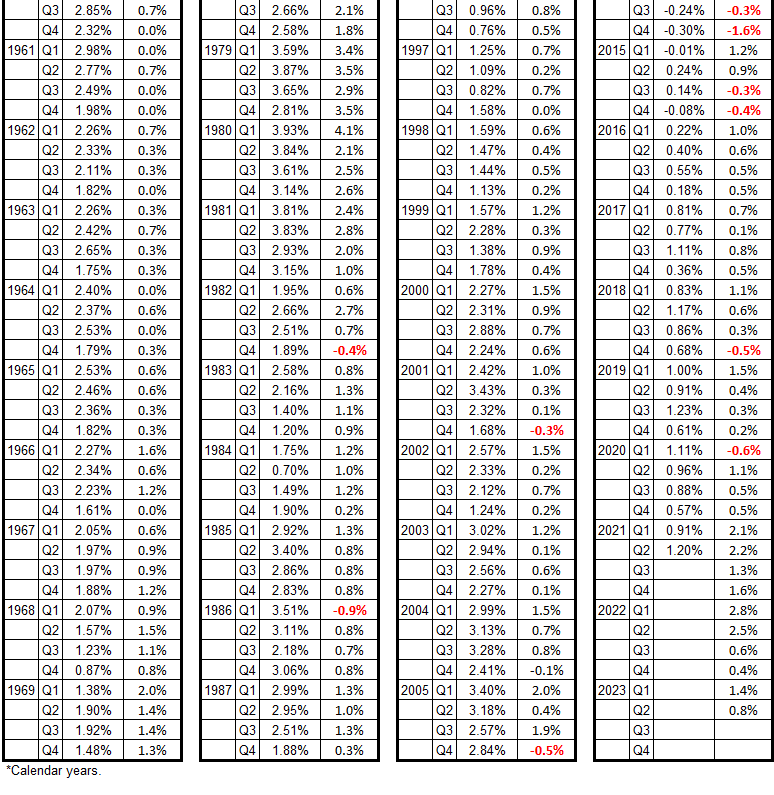

Table 9. Mortgage Debt Growth and Inflation (CPI), CPI Leads by 3 Months, 1952-2019*

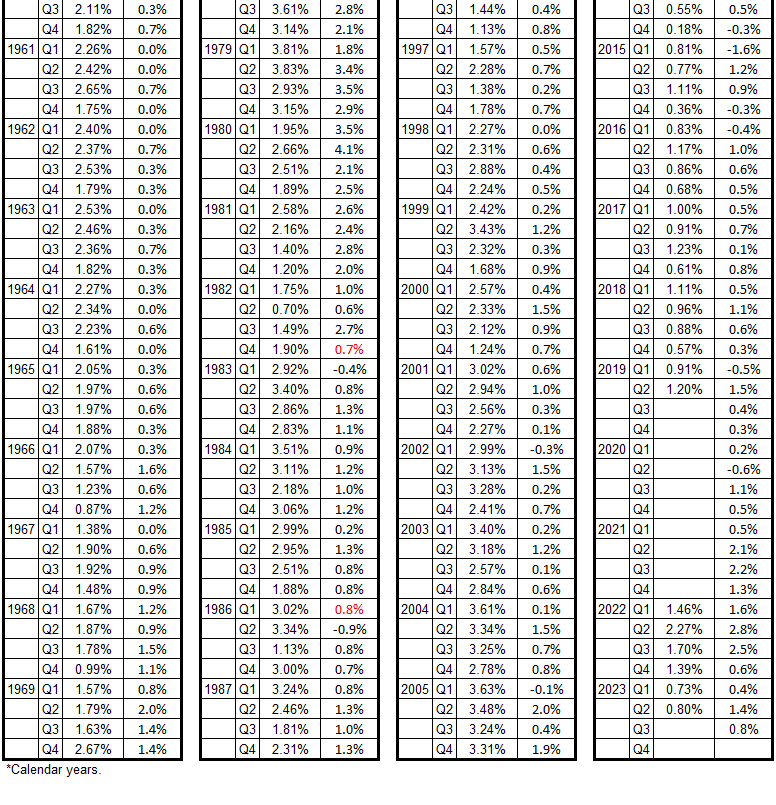

Table 10. Mortgage Debt Growth and Inflation (CPI), CPI Leads by 6 Months, 1952-2019*

Table 11. Mortgage Debt Growth and Inflation (CPI), CPI Leads by 9 Months, 1952-2019*

Table 12. Mortgage Debt Growth and Inflation (CPI), CPI Leads by 12 Months, 1952-2019*

Table 13. Mortgage Debt Growth and Inflation (CPI), CPI Leads by 18 Months, 1952-2019*

Table 14. Mortgage Debt Growth and Inflation (CPI), CPI Leads by 24 Months, 1952-2019*

Analysis

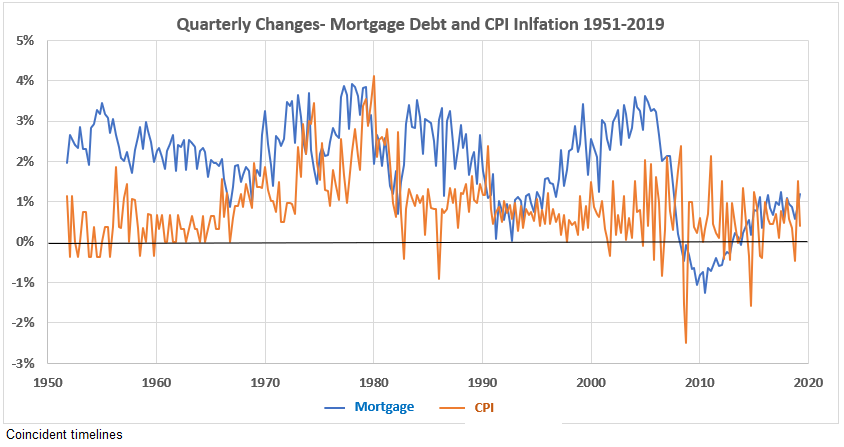

This data shows a complete lack of patterned structure. Figure 1 shows that the timeline variations for quarterly changes in Mortgage Debt and CPI Inflation show no consistent correlations. Over the long 67-year time frame, the two patterns seem to follow largely independent paths. This is true for changes over a few quarters and for long-term trends.

Figure 1. Quarterly Changes – Mortgage Debt and CPI Inflation 1951-2019

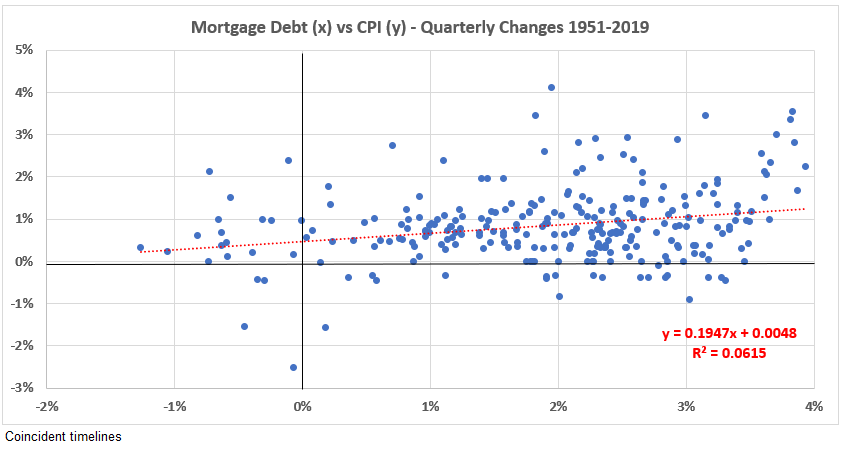

A scatter plot of the quarterly data with coincident timelines for the two variables (Figure 2) indicates a weak correlation ( R2 = 6.5%, R = 25%). The scatter diagram does not show the ideal oval football shape6 for the data points, so the result may not be reliable because the data is not well-behaved.

Figure 2. Scatter Diagram for Mortgage Debt – CPI Inflation Data Pairs 1951-2019, Coincident Timelines

We see no potential for useful correlation analysis in the entire data set. Further work will study what happens with the analysis of shorter time periods within the 67-year time frame.

Conclusion

The fine data granularity (more than 260 data point pairs) may provide useful information when various time periods are analyzed. We will look at the time periods for each of the three inflation behaviors shown in Table 1. As we have done before,1,2 timeline shifts will be examined to see if any information can be determined about possible cause-and-effect relationships. The next step in this process will be to analyze the positive inflation surges during the time interval 1952-2019.

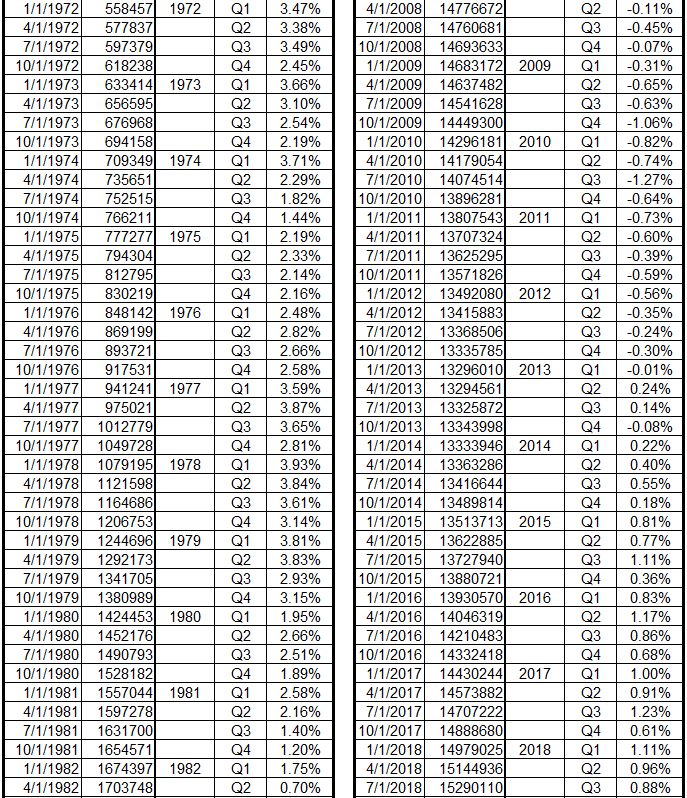

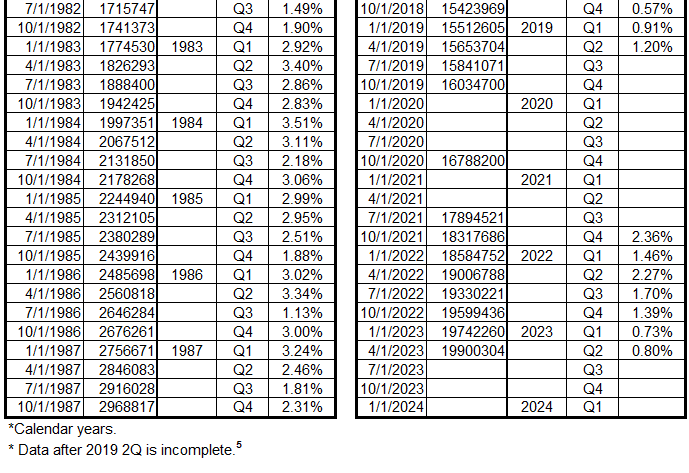

Appendix 1

The Mortgage Debt Outstanding is from Fed databases.4,5 The data after 2Q 2019 is incomplete.

Table A1. Growth Rate of Mortgage Debt 1952-2022* (Quarter-over-Quarter)

Appendix 2

The Consumer Price Index (CPI) data is from the Fed database.2 The table below shows the conversion of the Fed data to growth rate by quarter.

Table A2. Growth Rate of CPI 1913-2022* (Quarter-over-Quarter)

Footnotes

1. Lounsbury, John, “Government Spending and Inflation. Reprise and Summary”, EconCurrents, August 20, 2023. https://econcurrents.com/2023/08/20/government-spending-and-inflation-reprise-and-summary/.

2. Lounsbury, John, “Consumer Credit and Inflation: Part 4”, EconCurrents, September 23, 2023. https://econcurrents.com/2023/09/23/consumer-credit-and-inflation-part-4/.

3. Federal Reserve Economic Data, Consumer Price Index for All Urban Consumers: All Items in U.S. City Average, Index 1982-1984=100, Monthly, Not Seasonally Adjusted, https://fred.stlouisfed.org/graph/?id=CPIAUCNS.

4. Federal Reserve Economic Data, Mortgage Debt Outstanding, All holders (DISCONTINUED) (1949-2019), https://fred.stlouisfed.org/series/MDOAH.

5. Federal Reserve Economic Data, Mortgage Debt Outstanding, Millions of Dollars; End of Period, https://fred.stlouisfed.org/release/tables?rid=52&eid=1192326&od=2022-07-01#.

6. Lounsbury, John, “Government Spending and Inflation: Reprise and Summary,” EconCurrents, August 20, 2023. https://econcurrents.com/2023/08/20/government-spending-and-inflation-reprise-and-summary/

7. Freedman, David, Pisani, Robert, and Purves, Richard, Statistics, Fourth Edition, W.W. Norton & Company (New York) and Viva Books (New Delhi), 2009. See Chapters 8 & 9 for an explanation of how normal distributions relate to determining correlation coefficients. See p. 147 for a discussion of football-shaped scatter diagrams.