Note: A major addition was added to the conclusion at 1:43 a.m. EDT on October 23, 2023.

This article concludes the analysis of the correlation patterns between Mortgage Debt and Consumer Inflation (CPI). The last of the three types of inflation patterns (time periods with no significant inflation trends) is the subject of analysis here. The other two types of patterns (inflation surges1 and disinflation/deflation surges2) were analyzed previously. The conclusion discusses the correlation patterns for all time periods, looks for any common threads, and identifies important differences across time periods and types of correlation patterns.

From a photo by The Agent on Unsplash.

Introduction

The hypothesis we are testing is that inflation depends on mortgage debt in a linear manner, expressed in the following equation:3

I = mS + b

where

I = Change in CPI (the Consumer Price Index)

S = Change in Mortgage Debt

Data

The data sources and tables for Mortgage Debt and CPI are in Part 1.3 The timelines for the two data sets are also in Part 1, with coincident timelines and offsets by three and six months out to 24 months for Mortgage Debt changes coming before CPI and vice versa.

The inflation timeline3 from 1952 through 2022 is in Part 1. The inflation timeline uses year-over-year inflation calculated quarterly. Figure 1 shows the graph of inflation for the 1952-2022 time period3 (from Part 1).

Figure 1. CPI Rolling Four Quarter Inflation 1952-2022 with Significant Changes in Inflation Noted

(Each letter identifies the end of a significant move. An * identifies the end of an insignificant time period.)

Table 1 shows the data from Figure 1.

Table 1. Timeline of Inflation Data 1952-2022 (Previously Table 4*.4)

In Table 1, a black letter identifies a significant positive surge in inflation, a red letter for significant negative surges, and no letter for time periods with no significant changes in inflation.

Significant surges are changes in inflation ≥4% with no intervening countertrend moves >1.5%.

Analysis

There are 13 quarterly timeline alignments examined in each of the 5 time periods:

- Mortgage Debt and CPI Inflation quarters are coincident.

- Mortgage Debt leads and lags CPI Inflation by one quarter (±3 months)

- Mortgage Debt leads and lags CPI Inflation by two quarters (±6 months)

- Mortgage Debt leads and lags CPI Inflation by three quarters (±9 months)

- Mortgage Debt leads and lags CPI Inflation by four quarters (±12 months)

- Mortgage Debt leads and lags CPI Inflation by six quarters (±18 months)

- Mortgage Debt leads and lags CPI Inflation by eight quarters (±24 months)

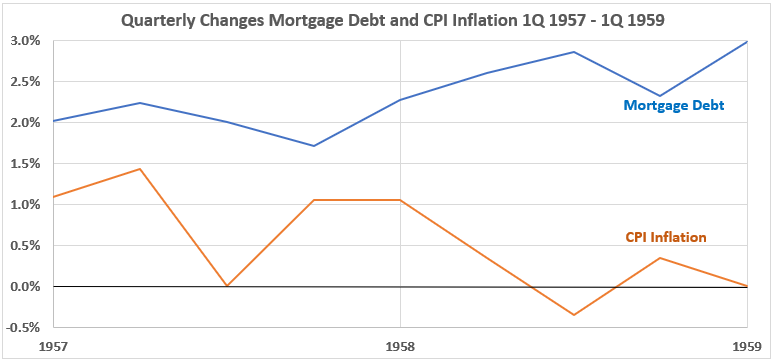

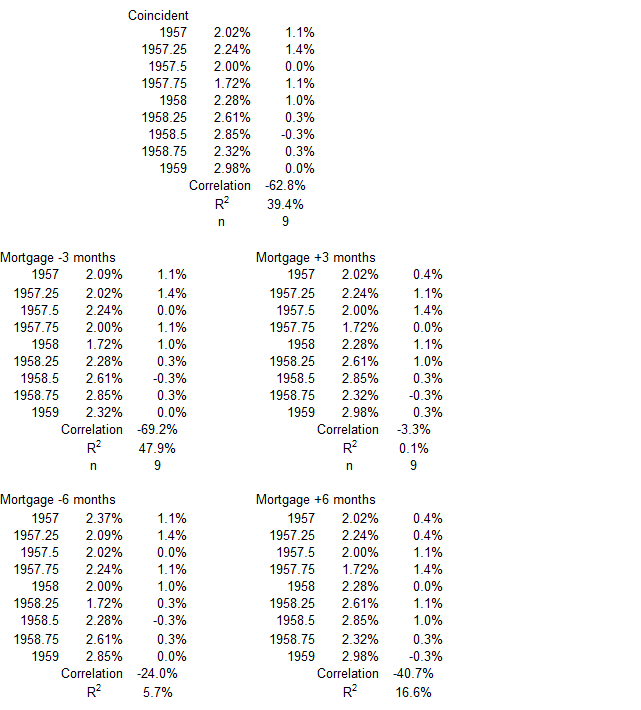

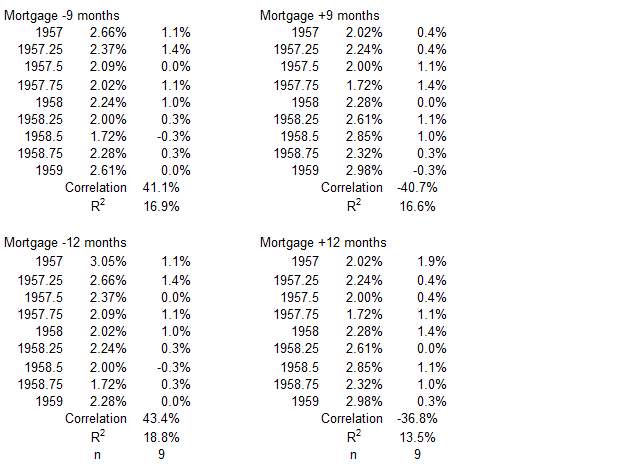

2Q 1957 – 1Q 1959

Figure 1. U.S. Mortgage Debt and Inflation 1Q 1957 – 1Q 1959

In this time period, CPI inflation quarterly changes are in a gradual declining trend. For Mortgage Debt, quarterly changes are mostly in an upward trend. The magnitude of the quarterly changes for Mortgage Debt are larger than for inflation, but inflation shows more volatility.

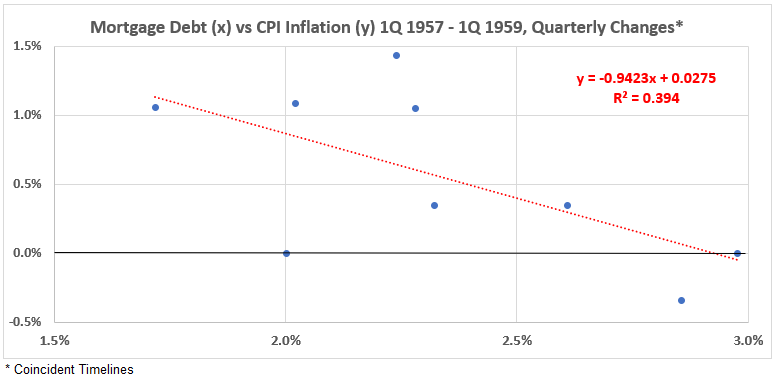

Figure 2. Quarterly Changes in Mortgage Debt (x) vs. CPI Inflation (y) 1Q 1957 – 1Q 1959

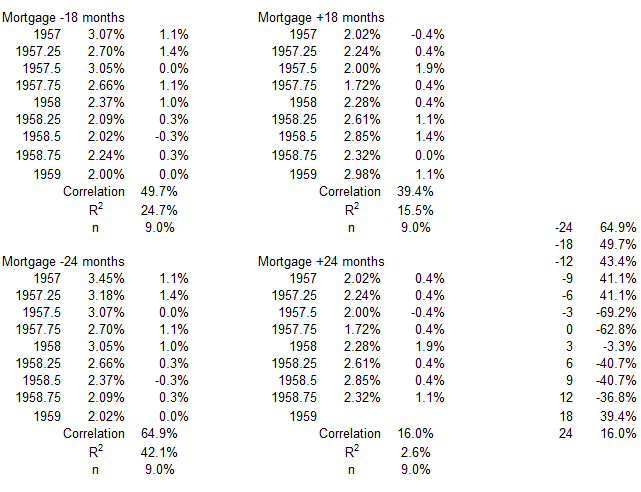

The association (correlation) between Mortgage Debt and CPI Inflation is moderately negative for this noninflationary period: R = –63%, R2 = 39%.

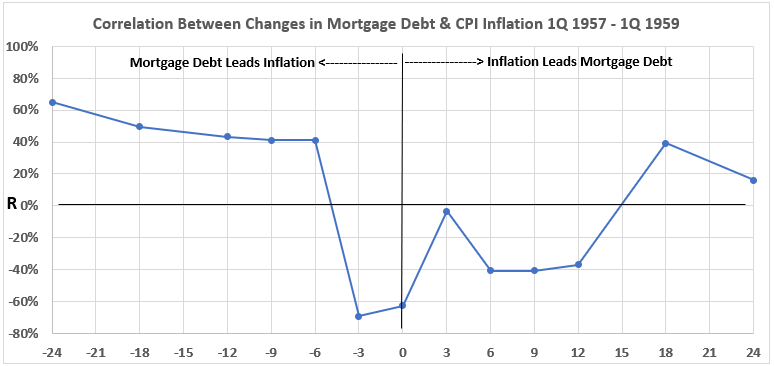

Figure 3. Correlation Between Mortgage Debt and CPI Inflation 1Q 1957 – 1Q 1959

Figure 3 shows the positive association of Mortgage Debt with inflation is moderate when Mortgage Debt comes before inflation by 6 months or more (left-hand side of the graph). On the other hand, the association is negative (mostly weakly) when inflation comes before credit spending by 3, 6, 9, and 12 months. With an 18- or 24-month lead, the association becomes weakly positive. This is similar to the pattern seen several times for positive and negative inflation surges.1,2

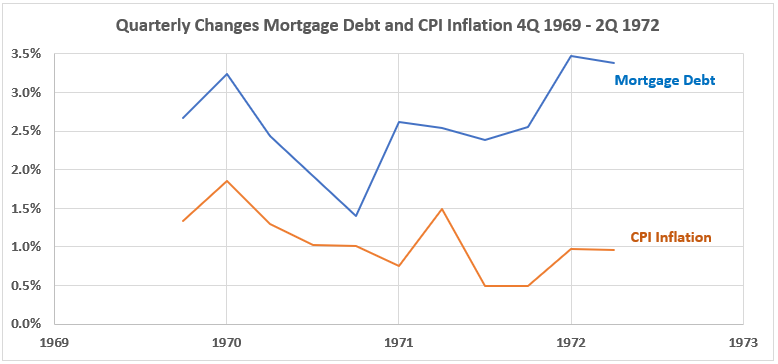

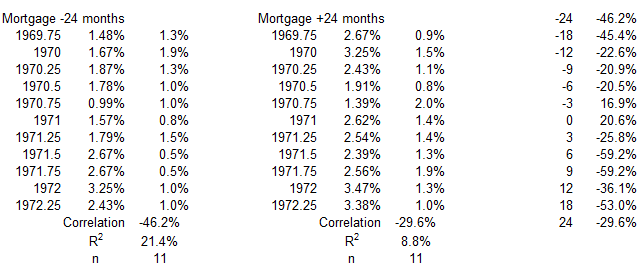

1Q 1970 – 2Q 1972

Figure 4. U.S. Mortgage Debt and Inflation 4Q 1969 – 2Q 1972

For inflation, Figure 4 is similar to Figure 1, with a gradually decreasing trend for quarterly inflation changes. The quarterly changes in Mortgage Debt show more volatility here than in Figure 1. Mortgage Debt changes from a trend of decreasing quarterly changes for the first four quarters to a trend of increasing changes.

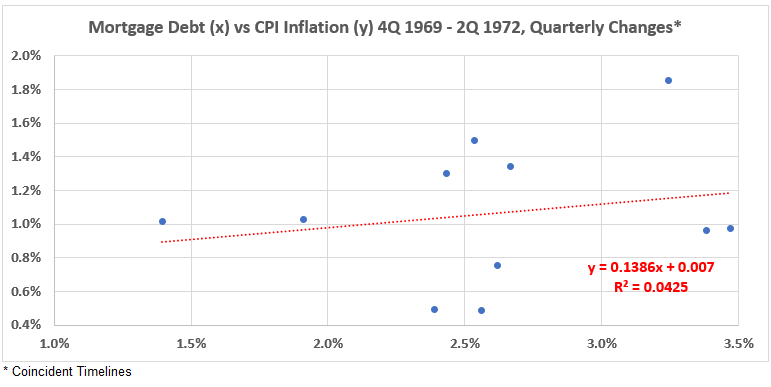

Figure 5. Quarterly Changes in Mortgage Debt (x) vs. CPI Inflation (y) 4Q 1969 – 2Q 1972

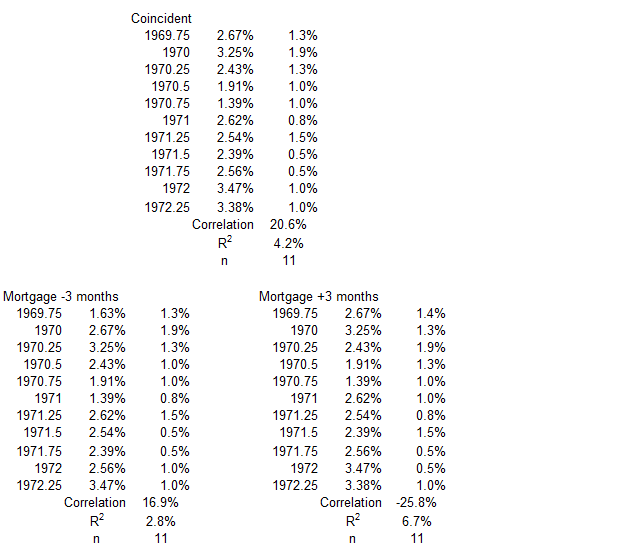

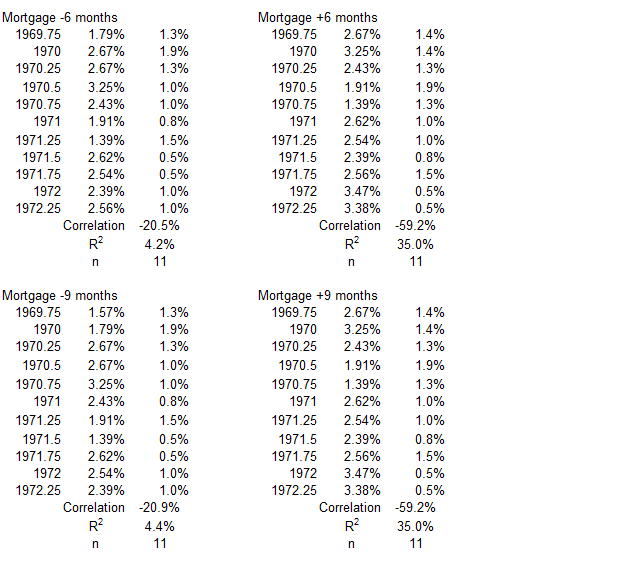

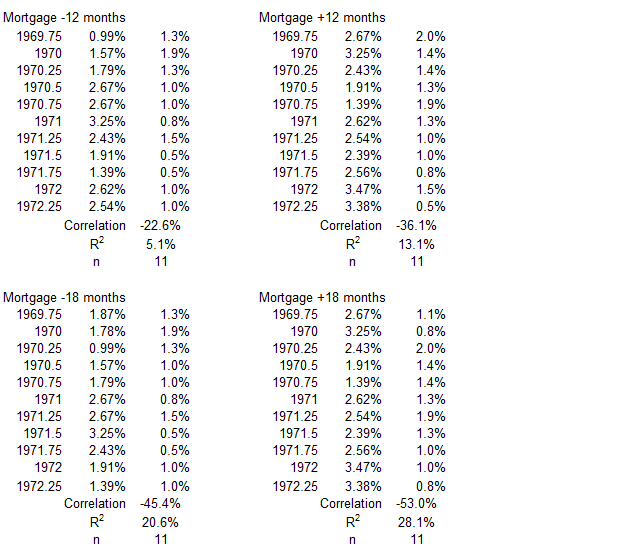

The association (correlation) between HNO Credit and CPI Inflation is weakly positive for this period: R = 21, R2 = 4.2%.

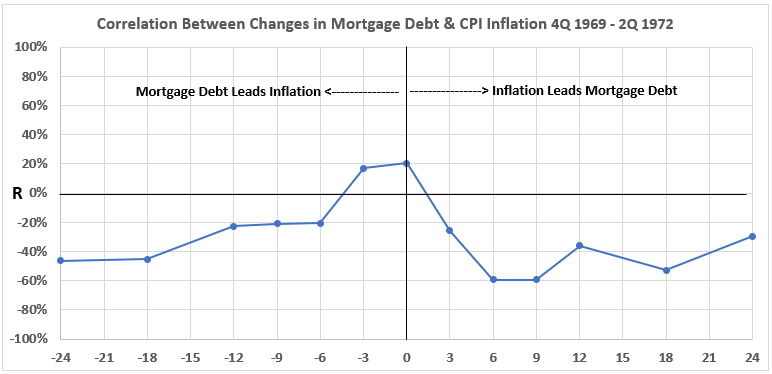

Figure 6. Correlation Between Mortgage Debt and CPI Inflation 4Q 1969 – 2Q 1972

Most of the associations here are weakly negative. The exceptions are Mortgage Debt coincident with and leading CPI by 3 months (weakly positive) and Inflation leading Mortgage Debt by 6 and 9 months (moderately negative). There is little chance that Mortgage Debt could have had any major cause-and-effect relationship with CPI Inflation during this period.

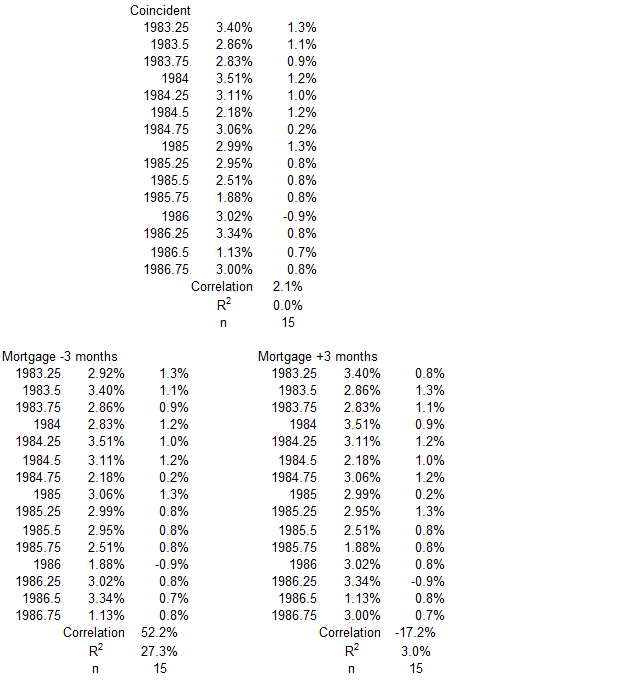

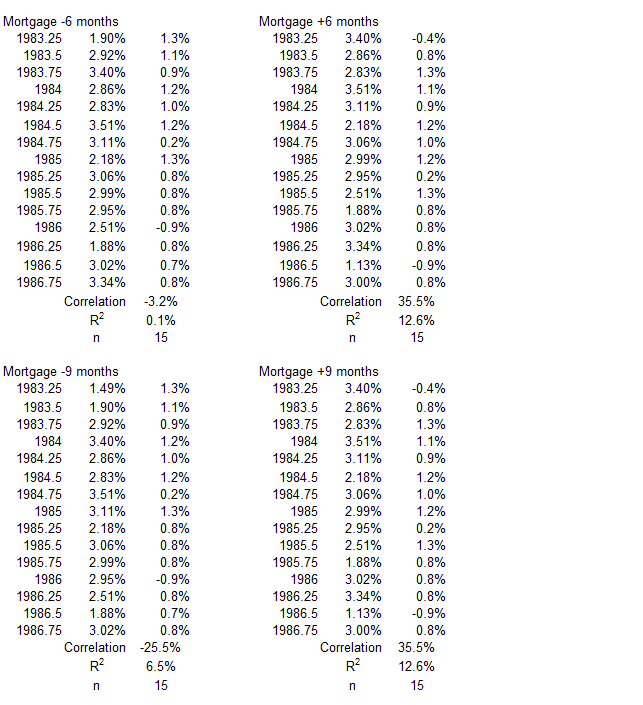

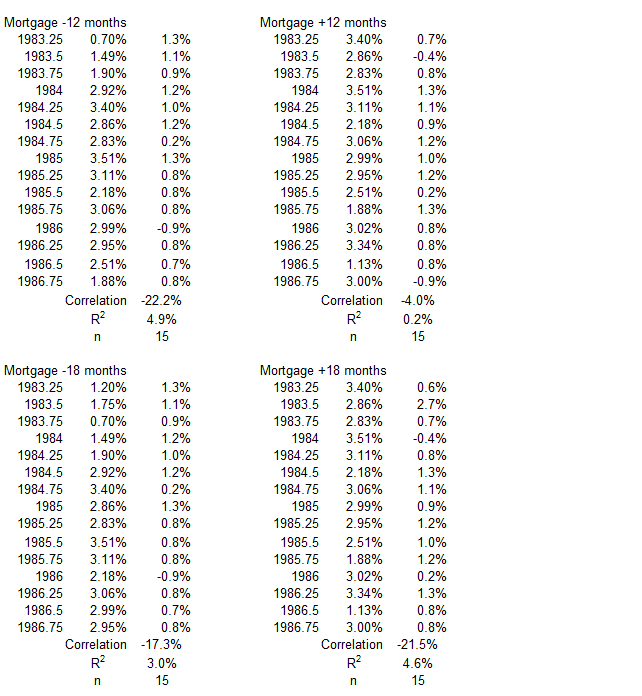

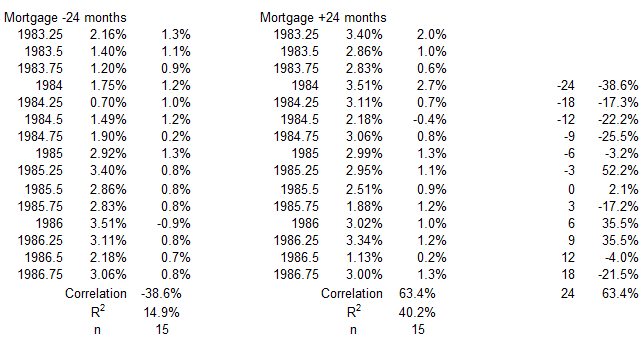

3Q 1983 – 4Q 1986

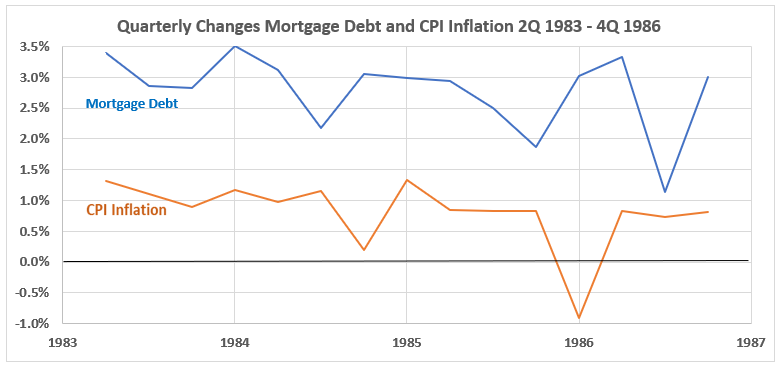

Figure 7. U.S. Mortgage Debt and Inflation 2Q 1983 – 4Q 1986

Figure 7 shows a different pattern than the two previous periods above. Here, the quarterly increases in Mortgage Debt are in a declining trend for 14 quarters, with higher volatility at the end. CPI Inflation shows a very slight decreasing quarterly change trend with little volatility except for 3Q – 4Q 1984 and 4Q 1985 – 1Q 1986. The other quarterly changes are close to 1%.

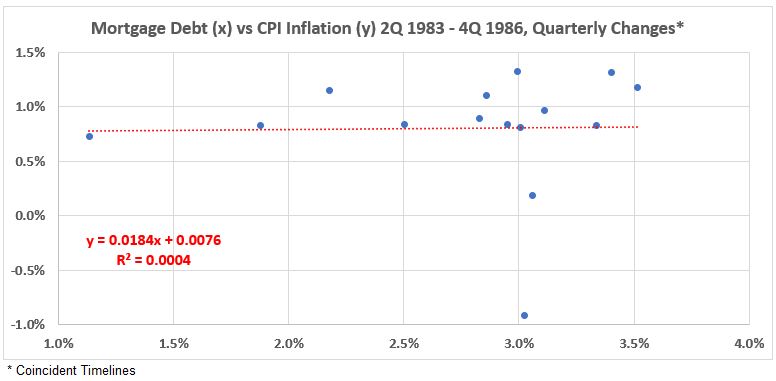

Figure 8. Quarterly Changes in Mortgage Debt (x) vs. CPI Inflation (y) 2Q 1983 – 4Q 1986

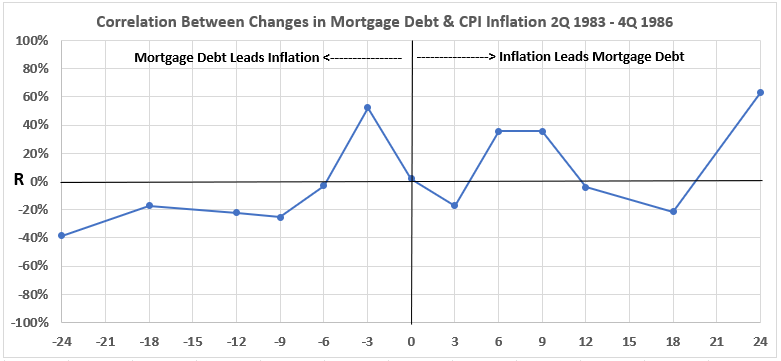

This time period differs from the first two, with R2 essentially zero. There is a slightly positive correlation: R = 2.1%

Figure 9. Correlation Between Mortgage Debt and CPI Inflation 2Q 1983 – 4Q 1986

The results in Figure 9 are similar to Figure 6 in that there are limited possibilities for cause-and-effect relationships.

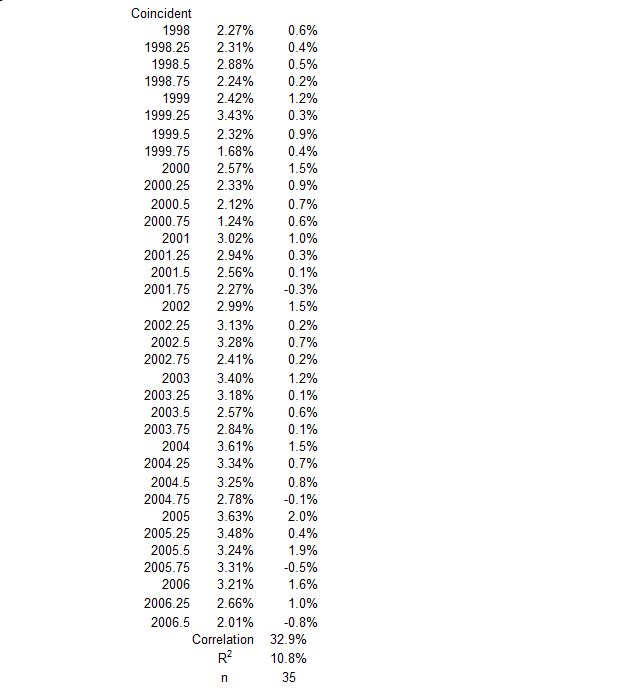

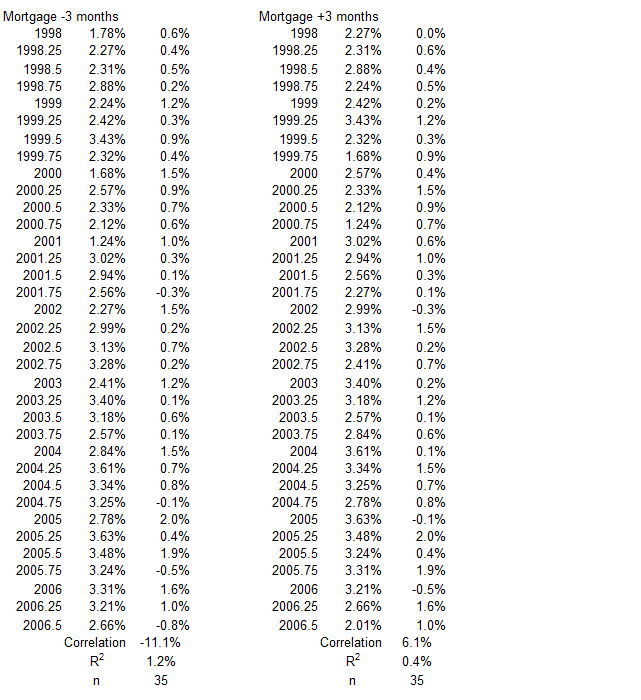

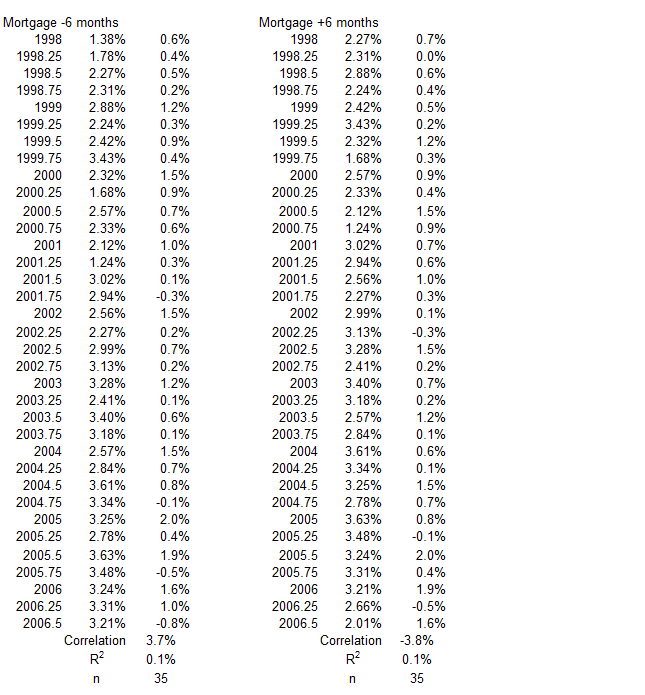

2Q 1998 – 3Q 2006

Figure 10. U.S. Mortgage Debt and Inflation 1Q 1998 – 3Q 2006

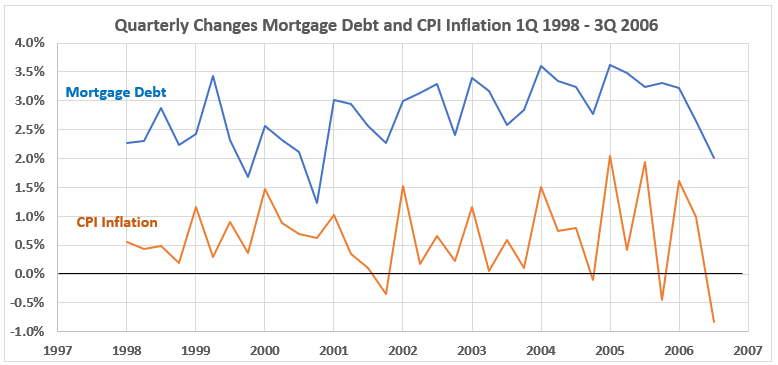

This period continues to show Mortgage Debt quarterly changes larger than CPI Inflation changes. Neither variable shows significant trending. CPI volatility is larger than Mortgage Debt, differing from the two immediately preceding periods and similar to the first period.

Figure 11. Quarterly Changes in Mortgage Debt (x) vs. CPI Inflation (y) 1Q 1998 – 3Q 2006

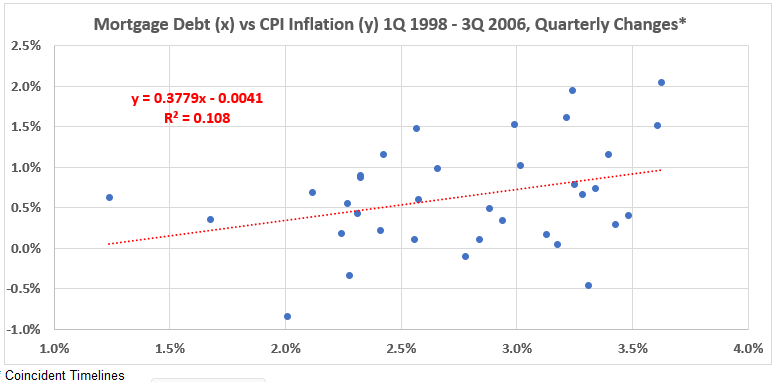

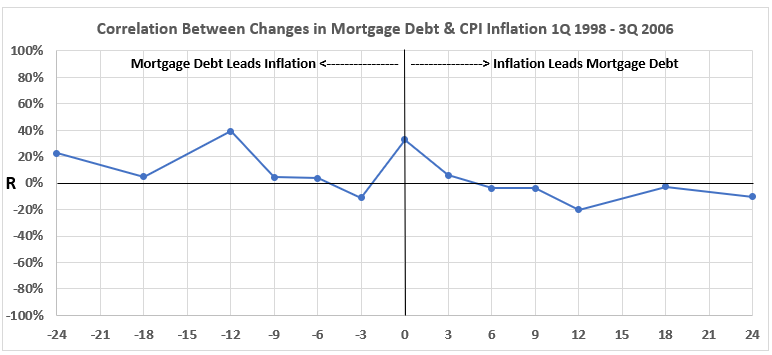

This data shows a weak positive correlation: R = 33%, R2 = 11%.

Figure 12. Correlation Between Mortgage Debt and CPI Inflation 1Q 1998 – 3Q 2006

Figure 12 is similar to Figures 6 and 9, showing little possibility for important cause-and-effect relationships between quarter changes in Mortgage Debt and CPI inflation.

3Q 2011 – 2Q 2019

The data set for this time period is truncated by four quarters because quarterly mortgage debt data was not found for 3Q 2019 – 2Q2020.

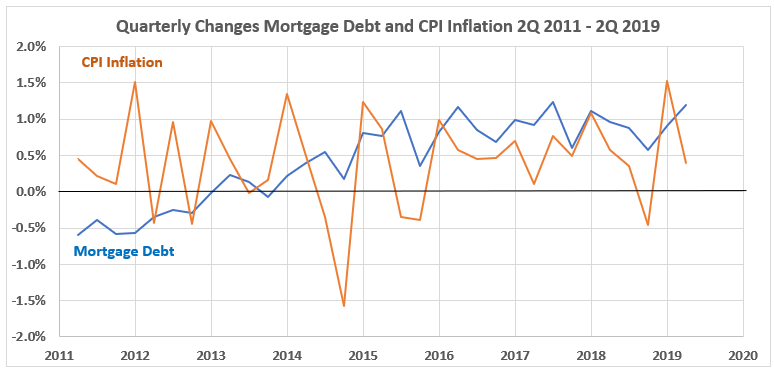

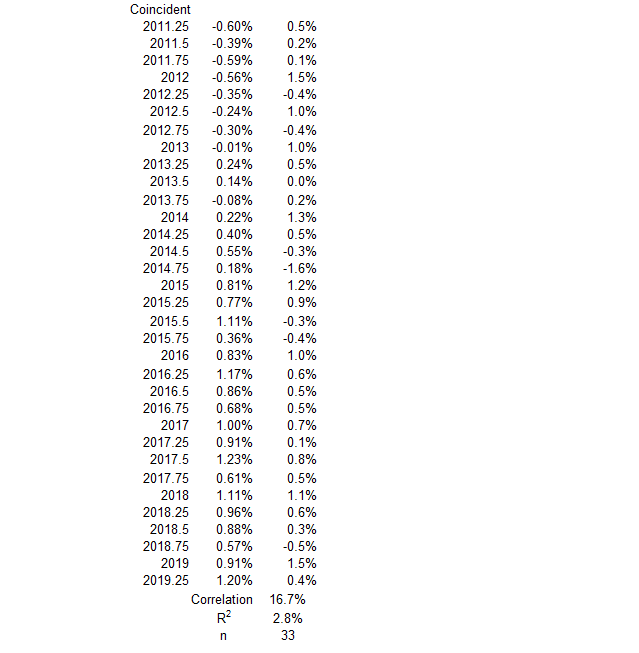

Figure 13. U.S. Mortgage Debt and Inflation 2Q 2011 – 2Q 2019

Figure 13 shows the only time that CPI Inflation quarterly changes have been larger than those for Mortgage Debt in this study of time periods without inflation surges – up or down. During this period, CPI Inflation quarterly change volatility was consistently larger than for Mortgage Debt changes. The trend for CPI is quite flat for this time period, while Mortgage Debt changes are trending higher for most of the period.

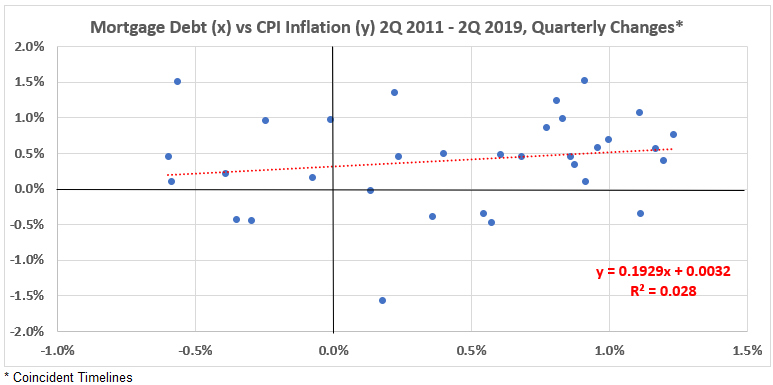

Figure 14. Quarterly Changes in Mortgage Debt (x) vs. CPI Inflation (y) 2Q 2011 – 2Q 2019

There is a very weak positive correlation for this time period: R = 17%, R2 = 3%. The two data points that look most like possible outliers are (0.18%, -1.6%) for 4Q 2014 and (-0.56%, 1.5%) for 1Q 2012. At this point, there is no reason to consider dismissing them. Such outliers are to be expected when one of the variables has extreme volatility, as inflation did during this time period.

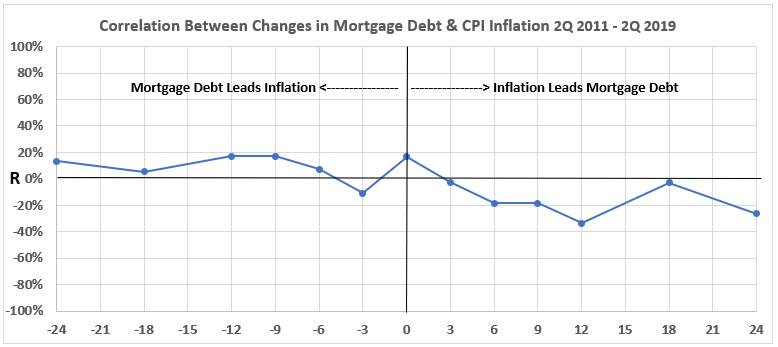

Figure 15. Correlation Between Mortgage Debt and CPI Inflation 2Q 2011 – 2Q 2019

Figure 15 shows the smallest possibility for cause-and-effect relationships in the five time periods analyzed here.

Conclusion

The conclusion is divided into three discussions. First, the analysis results are discussed for the current study of time periods without significant inflation surges up or down. The results of this study are compared to previous results: Consumer Credit and Inflation5 and Federal Deficit Spending and Inflation.6 Finally, there is an overall summary and a forward look to future work.

Patterns of Correlation for Periods without Significant Inflation Surges

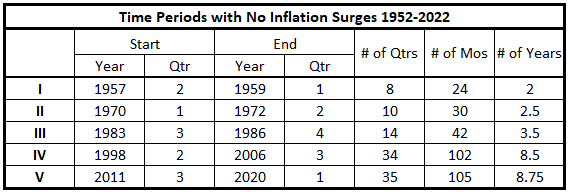

To simplify this discussion, the five periods without significant surges in inflation are numbered, as shown in Table 2.

Table 2. Time Periods with No Inflation/Disinflation Surges 1952-1022

There are fewer correlations found in this data than we might have expected. The correlations here are generally less remarkable than the somewhat unremarkable previous results for noninflationary periods. The general observations for the five periods analyzed in this article are:

- Inflation volatility quarter-to-quarter is much less for I, II, and II than for IV and V.

- Only in the first period (I) do we see the positive association between Mortgage Debt changes and following inflation changes that are more common with positive and negative inflation surges.

- Except for the first period, there are limited opportunities for possible important cause-and-effect relationships when there are no inflation/disinflation surges.

Overview of All Mortgage Debt Spending Data Sets

Let’s review the results for all 17 time periods – positive and negative inflation surges plus the periods without surges analyzed above. There are two patterns in the results that deserve commentary. We will briefly address each of them after discussing the general overview.

General Overview

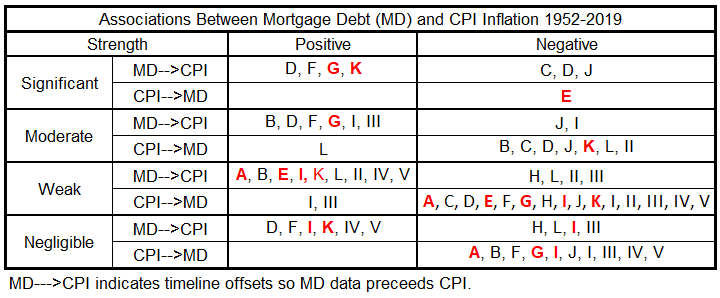

Table 3 summarizes the results for all time periods for correlation (association) of quarterly Mortgage Debt changes with CPI Inflation changes. In the table, black letters are for periods with positive inflation surges, red letters are for periods with negative inflation surges, and Roman numerals are for periods without surges.

Table 3. Associations Between Mortgage Debt (MD) and CPI Inflation 1952-2019

The associations shown in Table 3 indicate the maximum possible cause-and-effect relationships. The moderate correlation strength covers the range 50%>R2>25%. So, for example, R2 = 40%, no more than 40% 0f one variable can result from the other. But the lower limit of cause-and-effect is 0, depending on other information in addition to the statistical result. Stated differently, the cause of one variable is between 60% and 100% from factors other than the second variable.

The weak and negligible associations give a more satisfying result. They indicate that much (more than 75%) of the cause of one variable comes from other sources than the second (weak association), or nearly 100% comes from other sources (negligible).

There are some possibilities for more than 50% cause-and-effect (significant strength), but, without further information, proof is not given.

There are also possibilities for important cause-and-effect relationships between 25% and 50% (moderate strength). But additional information is needed in each case to prove that the causations are not much less.

Comparison to Results for Consumer Credit

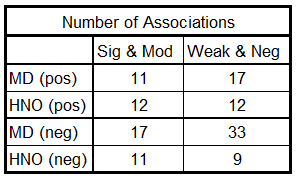

The results in Table 3 above can be compared to the results for the analysis of Consumer Credit data associations with CPI Inflation.5 Data from Table 3 in the Consumer Credit article is compared with data in the current Table 3, above. The results are in Table 4.

Table 4. Comparisons of Associations with CPI Inflation

for Consumer Credit (HNO) and Mortgage Debt (MD)

Only one comparison between the associations for the two variables is comparable: Significant and Moderate positive associations (11 for Mortgage Debt and 12 for Consumer Credit). The weak and negative associations are interesting because they indicate much less opportunity for cause-and-effect relationships for Mortgage Debt changes than for Consumer Credit.

The larger number of associations for Mortgage Debt changes with inflation may represent the greater sensitivity of mortgage debt spending to interest rate changes than is the case for Consumer Credit. See further discussion below.

Positive Correlations Between Mortgage Debt and Later Inflation

There are a number of cases where there are moderate (occasionally significant) correlations between quarterly changes for the two variables that drop significantly as the timeline offset gets closer to zero (coincidence). What could cause such a pattern? Why would a positive correlation disappear as the offset of timelines got smaller?

One possibility is that Mortgage Debt is not directly related to future CPI Inflation but only through an intermediary association. If Mortgage Debt was associated with some other factor in the first few quarters and then the other factor was associated with CPI Inflation in the following quarters, the pattern we have observed would be explained. We do not have enough work done yet to take a stab at looking for such “compounded associations.” For now, we take note of this and continue to collect more data and analysis.

Negative Correlations Between CPI Inflation and Later Mortgage Debt

There are many results showing negative associations: CPI Inflation changes with later Mortgage Debt changes. Some of these are weak or very weak correlations. In those cases, the weak correlations have value in a negative sense: They indicate that no important cause-and-effect relationships exist.

For those cases where the correlation is moderate, there is a possibility that important cause-and-effect relationships exist. Increasing CPI changes may cause decreasing Mortgage Debt changes. Also, decreasing CPI changes may cause increasing Mortgage Debt changes. Both postulates are reasonable when one considers how interest rates change during inflationary and disinflationary periods. However, the possibility is not proven without further information. The connection between correlation and probability simply defines case-and-effect to lie somewhere between the value of R2 and zero.

For more discussion on cause-and-effect limitations, refer back to the General Overview, above.

Comparison of Inflation Correlations for Federal Deficit Spending, Consumer Credit Spending, and Mortgage Debt Spending

The is not being pursued at this time. The previous deficit spending and inflation study was done using correlations between 12-month data points rather than quarterly.6 Quarterly correlations will be determined for federal deficit spending at some point, and then the comparison can be undertaken.

Summary

There are other sources of money creation than the two studied so far. Next, we will look at non-financial business debt, hopefully starting next week.

Appendix

The data sets for each of the periods without surging inflation or disinflation/deflation are below. They come from the tables of timeline aligments3 (Mortgage Debt and Inflation: Part 1).

2Q 1957 – 1Q 1959

1Q 1970 – 2Q 1972

3Q 1983 – 4Q 1986

2Q 1998 – 3Q 2006

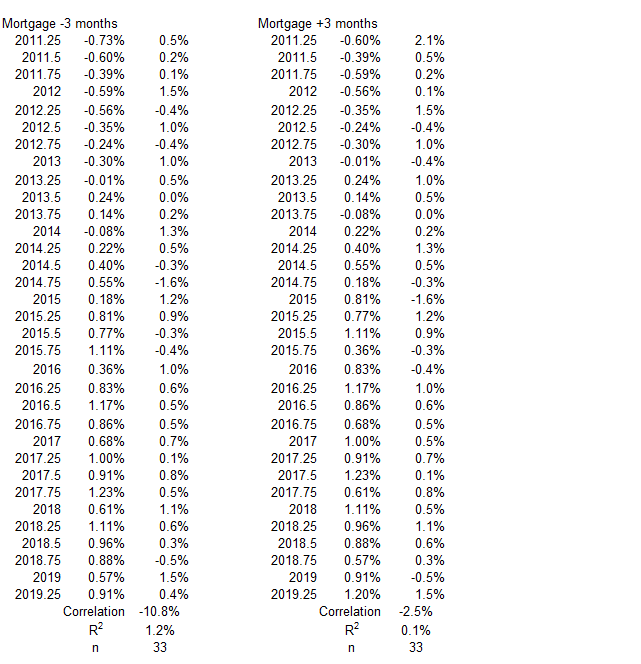

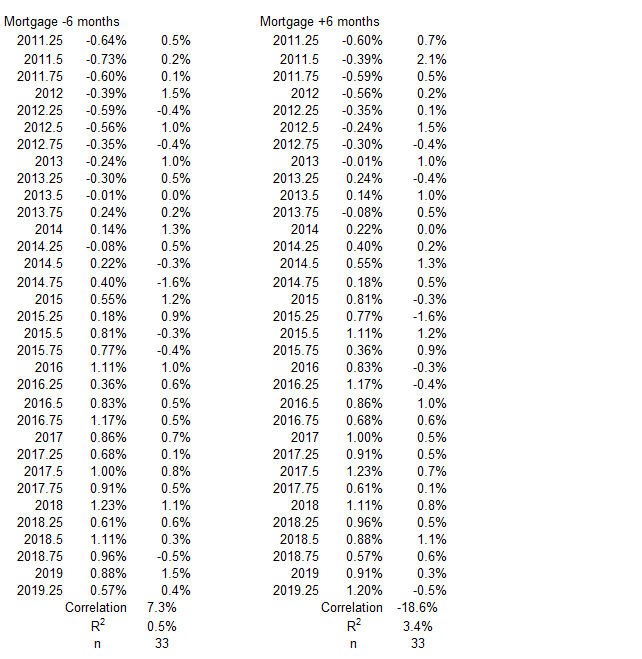

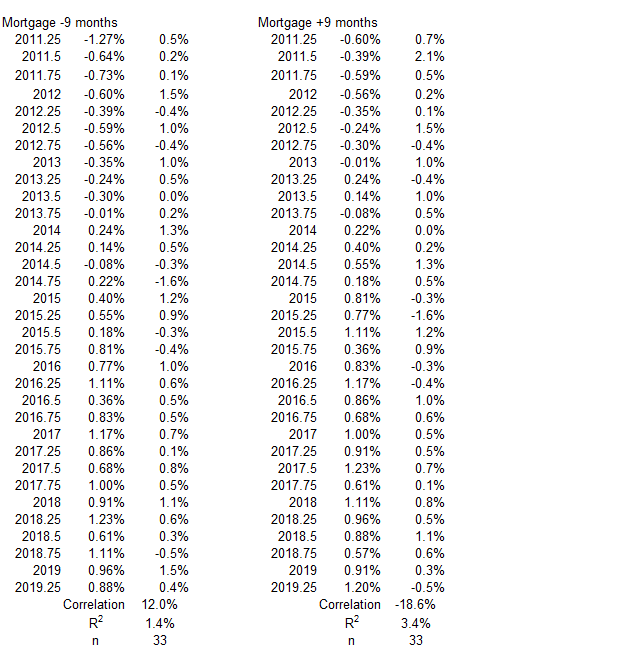

2Q 2011 – 2Q 2019

Footnotes

1. Lounsbury, John, “Mortgage Debt and Inflation: Part 2”, EconCurrents, October 8, 2023. https://econcurrents.com/2023/10/08/mortgage-debt-and-inflation-part-2/.

2. Lounsbury, John, “Mortgage Debt and Inflation: Part 3”, EconCurrents, October 15, 2023. https://econcurrents.com/2023/10/15/mortgage-debt-and-inflation-part-3/.

3. Lounsbury, John, “Mortgage Debt and Inflation: Part 1”, EconCurrents, October 1, 2023. https://econcurrents.com/2023/10/01/18942/.

4. Lounsbury, John, “Consumer Credit and Inflation: Part 1”, EconCurrents, September 3, 2023. https://econcurrents.com/2023/09/03/consumer-credit-and-inflation-part-1/.

5. Lounsbury, John, “Consumer Credit and Inflation: Part 4”, EconCurrents, September 23, 2023. https://econcurrents.com/2023/09/23/consumer-credit-and-inflation-part-4/.

6. Lounsbury, John, “Government Spending and Inflation: Reprise and Summary”, EconCurrents, August 20, 2023. https://econcurrents.com/2023/08/20/government-spending-and-inflation-reprise-and-summary/.