EconCurrents is transitioning to Substack in 2025. The existing newsletter will be discontinued no later than 01February2025 .

Note that the stock markets will not be open tomorrow. The stock markets and government offices will be closed on Thursday, January 9, 2025, in observance of a national day of mourning for former President Jimmy Carter. Therefore there will be no newsletter tomorrow.

Summary Of the Markets Today:

The Dow closed up 107 points or 0.25%,

Nasdaq closed down 11 points or 0.06%,

S&P 500 closed up 9 points or 0.16%,

Gold $2,681 up $15.50 or 0.590%,

WTI crude oil settled at $73 up $0.91 or 1.21%,

10-year U.S. Treasury 4.677 up 0.006 points or 0.128%,

USD index $109.01 up $0.47 or 0.43%,

Bitcoin $93,811 down $2,805 or 2.99%, (24 Hours),

*Stock data, cryptocurrency, and commodity prices at the market closing

Today’s Highlights – Market Summary

US stocks showed mixed performance on Wednesday as investors reacted to reports of President-elect Donald Trump potentially declaring a national economic emergency to implement proposed tariffs. The S&P 500 and Dow Jones Industrial Average saw slight gains, while the NASDAQ Composite closed marginally lower. The market was influenced by several key factors. Trump’s potential tariff plans: CNN reported that Trump is considering using emergency powers to enact his proposed tariff framework, which has caused some market uncertainty. Minutes from the Fed’s December meeting indicated support for a gradual pace of interest rate cuts in 2025. Recent strong economic indicators, including service sector growth and job openings, have raised concerns about persistent inflation. The 10-year Treasury yield remained around 4.7%, reflecting market expectations of potentially slower interest rate cuts. Private sector job growth slowed in December, but unemployment claims unexpectedly fell, suggesting a stable labor market. Investors are closely monitoring these developments as they assess the economic outlook and potential policy shifts under the incoming Trump administration.

Today’s Economic Releases Compiled by Steven Hansen, Publisher:

Private employers added 122,000 jobs in December 2024 according to ADP. Hiring slowed in several industries. Employment in manufacturing shrank for the third straight month. Pay gains continued to slow. Year-over-year pay for job stayers was up 4.6 percent. For job-changers, pay rose 7.1 percent. Most of this year, one month ADP has higher employment gains – then the next month, the BLS has higher gains,. If this pattern continues – the BLS employment gains in December will be less than 122,000. But 122,000 is far from stellar growth, and below the growth necessary to employ new entrants to the labor force. According to Nela Richardson, Chief Economist, ADP:

The labor market downshifted to a more modest pace of growth in the final month of 2024, with a slowdown in both hiring and pay gains. Health care stood out in the second half of the year, creating more jobs than any other sector.

November 2024 sales of merchant wholesalers were up 0.9% from the revised November 2023 level. Total inventories were up 0.8% from the revised November 2023 level. The November inventories/sales ratio for merchant wholesalers was 1.33. The November 2023 ratio was 1.35. I am sure that NOBODY in government knows really what a wholesaler is – and the statistics are likely garbage. The inventory to sales ratios are little changed which normally indicates there is no inventory gain (which is a sign of recession).

In the week ending January 4, the advance figure for seasonally adjusted initial unemployment claims 4-week moving average was 213,000, a decrease of 10,250 from the previous week’s unrevised average of 223,250. The unemployment claims are low historically and consistent with a growing economy.

The Federal Open Market Committee (FOMC) meeting in December 2024 provided updated economic projections and insights into monetary policy decisions. Note that I do not believe inflation is under control as any new development could set off another round of inflation. Key points include:

Economic Projections

Real GDP growth: Median projection revised upward to 2.5% for 2024 and 2.1% for 2025.

Unemployment rate: Projected to be 4.2% in 2024, slightly lower than previous estimates.

Inflation: PCE inflation projections raised for 2024 (2.4%) and 2025 (2.5%).

Monetary Policy

The federal funds rate was lowered by 25 basis points to a range of 4.25% to 4.5%.

FOMC members anticipate two 25 basis point rate cuts in 2025, totaling 50 basis points.

The median projection for the federal funds rate at the end of 2025 is now 3.9%, up from 3.4% in September.

Economic Outlook

Inflation is expected to continue moving towards the 2% target, but the process may take longer than previously anticipated. Several participants observed that the disinflationary process may have stalled temporarily or noted the risk that it could.

Economic activity continues to expand at a solid pace, with consumer spending stronger than expected. Participants believe the strength of economic activity was unlikely to be a source of upward inflation pressures.

Labor market conditions are gradually easing while remaining solid overall.

Risks and Uncertainties

Upside risks to inflation have increased due to recent higher-than-expected readings and potential policy changes.

Uncertainties remain regarding the effects of potential changes in trade and immigration policies – bottom line they were worried about Trump.

The Committee views risks to its dual mandate objectives as roughly balanced.

The FOMC indicated a cautious approach to future policy decisions, emphasizing the need to carefully assess evolving economic conditions and maintain flexibility in monetary policy adjustments.

According to the Federal Reserve, “In November, consumer credit decreased at a seasonally adjusted annual rate of 1.8 percent. Revolving credit decreased at an annual rate of 12 percent, while nonrevolving credit increased at an annual rate of 2 percent.” Two things: 1) this data is not inflation adjusted and at least 2% should be subtracted from growth for inflation; and 2) I prefer year-over-year analysis which shows total consumer credit is up 1.7% year-over-year with components revolving credit (credit cards) up 3.6% year-over-year and nonrevolving credit (like car loans and student loans) up 1.0% year-over-year. The trend lines show less and less reliance on credit for consumer spending which constrains consumer spending.

Here is a summary of headlines we are reading today:

New Railway to Connect China, Kyrgyzstan, and Uzbekistan

Taliban Takeover of Afghanistan Fuels Militancy in Pakistan

Chevron Targets $6-8 bln In Free Cash Flow Growth By 2026

DOE Issues $1.8B Loan Guarantee To Arizona Utility For Renewable Energy

Guyana’s Crude Oil Exports Surged by 54% in 2024

Higher Taxes Could Slow China’s Fuel Oil Imports

Trump Not Ruling Out Force in Threats to Take Over Panama Canal

Nvidia’s Jensen Huang is ‘dead wrong’ about quantum computers, D-Wave CEO says

First major stock benchmark nears correction as small-cap Russell 2000 trade unravels

Judge approves Tesla directors’ nearly $1 billion deal to end excess pay case

Bitcoin falls to $94,000, giving back most of 2025’s early gains: CNBC Crypto World

This January indicator is an ‘early warning system’ for how the year will go

FOMC Minutes Show ‘Almost All’ Fed Members See Higher Inflation Risks, Cite Trump Policies

Most Fed officials were worried about higher inflation, but not enough to put rate hikes on the table, minutes of December meeting show

Click on the “Read More” below to access these, other headlines, and the associated news summaries moving the markets today.

EconCurrents is transitioning to Substack in 2025. The existing newsletter will be discontinued no later than 01February2025 .

Summary Of the Markets Today:

The Dow closed down 178 points or 42%,

Nasdaq closed down 375 points or 1.89%,

S&P 500 closed down 66 points or 1.11%,

Gold $2,665 up $17.30 or 0.065%,

WTI crude oil settled at $74 up $0.71 or 0.95%,

10-year U.S. Treasury 4.693 up 0.077 points or 1.668%,

USD index $108.67 up $0.42 or 0.38%,

Bitcoin $96,810 down $5,363 or 5.54%, (24 Hours),

*Stock data, cryptocurrency, and commodity prices at the market closing

Today’s Highlights – Market Summary

US stocks closed lower on Tuesday, reversing early gains as investors reassessed economic data and Federal Reserve rate cut expectations. The 10-year Treasury yield rose about 7 basis points to just below 4.7%. Key economic data releases influenced market sentiment: The ISM manufacturing PMI showed continued expansion, but the prices paid index jumped to a nearly two-year high of 64.4, raising inflation concerns. JOLTS job openings increased more than expected in November, while hiring slowed and the quits rate decreased. These reports led investors to push back expectations for Fed rate cuts, with traders now placing a less than 50% chance of a cut before June 2025. NVIDIA, which had reached a record close on Monday, reversed course and fell over 6%, becoming the Dow’s worst performer despite CEO Jensen Huang’s CES keynote unveiling new AI products. The labor market showed signs of cooling, with the hiring rate falling to 3.3% and the quits rate dropping to 1.9%, both now lower than pre-pandemic levels. This data suggests a “no hire, no fire” labor market environment, according to Oxford Economics. Investors are now looking ahead to Friday’s December jobs report for further insights into the labor market and potential implications for Fed policy.

Today’s Economic Releases Compiled by Steven Hansen, Publisher:

November 2024 exports were up 5.7% year-over-year while imports were up 8.1% year-over-year – the trade balance worsened by 20.8% year-over-year. The trend lines continue to show a an ever worsening trade balance with no end in sight.

The number of private job openings grew modestly from 6.9 million to 7.2 million on the last business day of November 2024. Studies by the Philly Fed have shown no correlation to economic or jobs growth with the hires and separations portion of JOLTS. I would expect a reasonably good jobs report (compared to the growth seen in 2024) this Friday based on this JOLTS data.

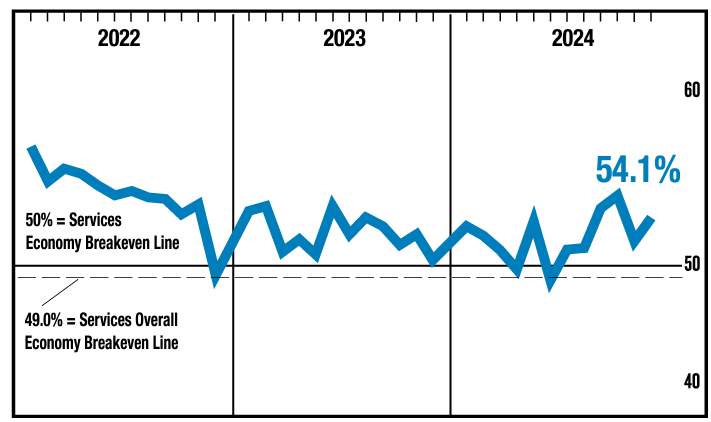

In December 2024, the ISM Services PMI® registered 54.1%, 2 percentage points higher than November. The Business Activity sub-index registered 58.2% in December, 4.5 percentage points higher than November. The New Orders sub-index recorded a reading of 54.2% , 0.5 percentage point higher than November. For the last 2 years, this index has generally remained in a tight band. As the U.S. is a services economy – this reading suggests little change in economic growth.

Home prices nationwide, including distressed sales, increased year over year by 3.4% in November 2024 compared with November 2023. On a month-over-month basis, home prices increased by 0.06% in November 2024 compared with October 2024. The CoreLogic HPI Forecast indicates that home prices will increase by 3.8% on a year-over-year basis from November 2024 to November 2025.

Here is a summary of headlines we are reading today:

Trump Pledges Swift Reversal of Biden’s Offshore Drilling Ban

Is U.S. Nuclear Power at Risk? Russia’s Uranium Restrictions Explained

EconCurrents is transitioning to Substack in 2025. The existing newsletter will be discontinued no later than 01February2025 .

Summary Of the Markets Today:

The Dow closed down 26 points or 0.06%,

Nasdaq closed up 243 points or 1.24%,

S&P 500 closed up 33 points or 0.55%,

Gold $2,645 down $9.90 or 0.037%,

WTI crude oil settled at $73 down $0.55 or 0.74%,

10-year U.S. Treasury 4.620 up 0.025 points or 0.544%,

USD index $108.26 down $0.69 or 0.63%,

Bitcoin $102,322 up $4,216 or 4.12%, (24 Hours),

*Stock data, cryptocurrency, and commodity prices at the market closing

Today’s Highlights – Market Summary

US stocks rose on Monday, led by a rally in chip stocks. The S&P 500 and the Nasdaq Composite climbed while the Dow Jones Industrial Average dipped marginally. The tech sector drove gains, with Nvidia shares rising over 3% to a record high and Micron Technology surging more than 10%. The rally was fueled by optimism around AI-driven growth after NVIDIA server partner Foxconn reported record revenue and a strong sales forecast. Investors are now anticipating Nvidia CEO Jensen Huang’s keynote speech at the CES tech conference for updates on the company’s new Blackwell chip. Disney confirmed plans to merge its Hulu + Live TV business with FuboTV, sending Fubo shares soaring nearly 250%. Bitcoin prices traded above $102,000 per token, surpassing $100,000 for the first time since December 19. The 10-year Treasury yield rose slightly. The US dollar index dropped sharply following reports of potential limited tariffs under the incoming Trump administration, but later pared some losses after Trump disputed the report. Markets will be closed on Thursday to mourn the death of former President Jimmy Carter, with attention focused on the release of December nonfarm payrolls data on Friday. In international news, Canadian Prime Minister Justin Trudeau resigned as Liberal Party leader, potentially reshaping Canada’s trade relationship with the US under a second Trump administration.

EconCurrents is transitioning to Substack in 2025. The existing newsletter will be discontinued no later than 01March2025 . All newsletter subscribers need to sign up for the EconCurrents Substack’s Newsletter by [clicking here].

Summary Of the Markets Today:

The Dow closed up 340 points or 0.80%,

Nasdaq closed up 341 points or 1.77%,

S&P 500 closed up 74 points or 1.26%,

Gold $2,651 down $18.00 or 0.670%,

WTI crude oil settled at $74 up $0.86 or 1.18%,

10-year U.S. Treasury 4.602 up 0.027 points or 0.590%,

USD index $108.92 down $0.48 or 0.44%,

Bitcoin $98,236 up $1,041 or 1.06%, (24 Hours),

Baker Hughes Rig Count: U.S. unchanged at 589 Canada -1 to 94

U.S. Rig Count is unchanged from last week at 589 with oil rigs down 1 to 482, gas rigs up 1 to 103 and miscellaneous rigs unchanged at 4.

*Stock data, cryptocurrency, and commodity prices at the market closing

Today’s Highlights – Market Summary

US stocks rebounded on Friday, ending a five-day losing streak and closing the first week of 2025 on a positive note. Despite this rally, all three major indexes finished the holiday-shortened week with losses, with the S&P 500 and Dow dropping over 1% and the NASDAQ declining 2%. Tesla shares surged 8% after reporting record-high sales in China for 2024. Nvidia stock climbed more than 4%, continuing its strong performance. US Steel stock fell 5% after President Biden blocked Nippon Steel’s $14.9 billion takeover bid. The ISM Manufacturing PMI rose to 49.3% in December, showing a slight improvement in the manufacturing sector but still indicating contraction. In political news, Mike Johnson was reelected as House speaker after promising to work with Elon Musk’s “Department of Government Efficiency” (DOGE) to address government spending and reform. Despite Friday’s gains, the much-anticipated “Santa Claus” rally failed to materialize, potentially impacting market sentiment for January and the year ahead.

Today’s Economic Releases Compiled by Steven Hansen, Publisher:

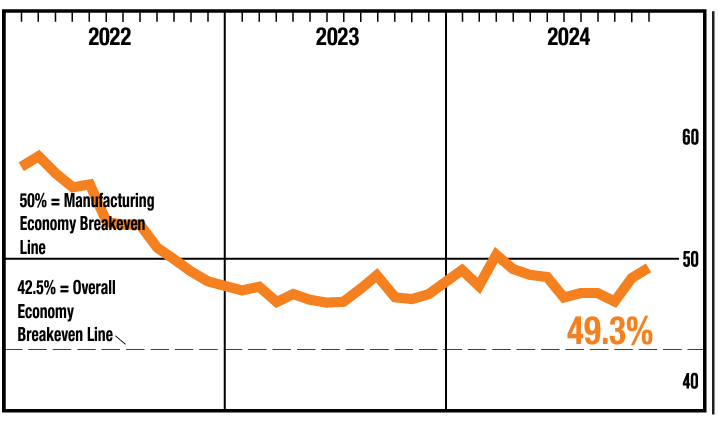

The Institute of Supply Management Manufacturing PMI® was 49.3% in November – 0.9 percentage points higher compared to November. The New Orders Index continued in expansion territory for the second month after seven months of contraction, strengthening to 52.5 percent, 2.1 percentage points higher than the 50.4 percent recorded in November. The December reading of the Production Index (50.3 percent) is 3.5 percentage points higher than November’s figure of 46.8 percent. The bottom line is that manufacturing continues in contraction according to this survey – although not by much.

Here is a summary of headlines we are reading today:

U.S. Drillers Start Out The New Year With A Whimper

EV Sales Rise as Trump Threatens to End Tax Credits

Moldova’s Breakaway Region Idles Industry Without Russian Gas

Uranium Spot Prices Set for Recovery in 2025

Middle East Crude Prices Surge as Supply From Iran and Russia Falls

Microsoft expects to spend $80 billion on AI-enabled data centers in fiscal 2025

S&P 500, Nasdaq snap five-day losing streak, but still close lower on the week: Live updates

GM, Ford report best annual U.S. sales since 2019

It’s time to boost 401(k) plan contributions for 2025 — here’s how much more you can save

‘Over 800 Biases Uncovered’ As Pentagon Ends AI Chatbot Pilot Program For Military Medicine

Treasury yields end higher after ISM’s stronger-than-expected manufacturing data

Oil prices score weekly gains, buoyed by China policy support

Click on the “Read More” below to access these, other headlines, and the associated news summaries moving the markets today.

EconCurrents is transitioning to Substack in 2025. The existing newsletter will be discontinued no later than 01March2025 . All newsletter subscribers need to sign up for the EconCurrents Substack’s Newsletter by [clicking here].

Summary Of the Markets Today:

The Dow closed down 152 points or 0.36%,

Nasdaq closed down 30 points or 0.16%,

S&P 500 closed down 13 points or 0.22%,

Gold $2,673 up $32.60 or 1.190%,

WTI crude oil settled at $73 up $1.35 or 1.88%,

10-year U.S. Treasury 4.559 down 0.018 points or 0.039%,

USD index $109.27 up $0.78 or 0.72%,

Bitcoin $97,101 up $1,771 or 2.64%, (24 Hours),

*Stock data, cryptocurrency, and commodity prices at the market closing

Today’s Highlights – Market Summary

Stock markets experienced a volatile start to 2025, with major indexes erasing earlier gains and ending the first trading day lower. Tesla shares slumped nearly 6% after reporting lower vehicle deliveries. Apple dropped over 2.5% due to price discounts in China. The market came off a strong 2024, with the S&P 500 achieving two consecutive years of over 20% gains. The US Dollar Index rose above 109, reaching its highest level since November 2022. Investors are cautiously optimistic about 2025, with Bank of America suggesting potential for a 10% return in the next 12 months, though the extraordinary 20%+ annual returns of recent years may be behind us. The trading day reflected ongoing market uncertainty, with initial optimism giving way to declines, particularly in technology and electric vehicle stocks.

Today’s Economic Releases Compiled by Steven Hansen, Publisher:

Construction spending during November 2024 is 3.0% above November 2023. Spending on private construction is up 2.5% year-over-year and public construction is up 4.6% year-over-year. Note in the graph below that for the last year, construction spending growth has been moderating. Construction spending has been a major bright spot in the economy – and that bright spot is becoming dim.

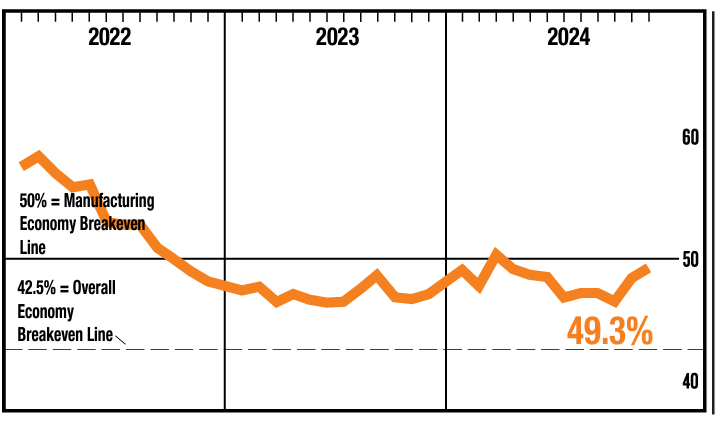

The Institute of Supply Management Manufacturing PMI® was 48.4% in November – 1.9 percentage points higher compared to October. The New Orders Index returned to expansion, albeit weakly, after seven months of contraction, registering 50.4 percent, 3.3 percentage points higher than the 47.1 percent recorded in October. The November reading of the Production Index (46.8 percent) is 0.6 percentage point higher than October’s figure of 46.2 percent. The bottom line is that manufacturing continues in contraction according to this survey/

In the week ending December 28, the advance figure for seasonally adjusted initial unemployment claims 4-week moving average was 223,250, a decrease of 3,500 from the previous week’s revised average. The previous week’s average was revised up by 250 from 226,500 to 226,750. This data is consistent with an expanding economy.

Here is a summary of headlines we are reading today:

What Next for US LNG After Ukraine Gas Transit Halts?

India’s Steel Industry Threatened by Record Chinese Imports

Dallas Survey: The Oil & Gas Outlook Is Finally Improving

Oil Rallies Despite Large Jump in Fuel Inventories

Tesla Stock Dips as Annual Deliveries See First Decline Since 2011

89% of New Cars Sold in Norway Last Year Were EVs

Stocks close lower in volatile start to 2025 as S&P 500 losing streak grows: Live updates

Meta replaces Global Affairs President Nick Clegg with Joel Kaplan ahead of Trump inauguration

Warren Buffett’s Berkshire Hathaway beats S&P 500 in 2024, posts 9th straight up year

Regulatory clarity could drive bitcoin to $225,000 this year, says H.C. Wainwright

Mortgage demand dives nearly 22% to end 2024

Officials ID person who rented Cybertruck used in explosion outside of Las Vegas Trump hotel

Cryptocurrencies jump to start 2025, bitcoin rises back above $97,000

10-year Treasury yield ends not far from 7-month high as new trading year begins

Click on the “Read More” below to access these, other headlines, and the associated news summaries moving the markets today.

EconCurrents is transitioning to Substack in 2025. The existing newsletter will be discontinued no later than 01March2025 . All newsletter subscribers need to sign up for the EconCurrents Substack’s Newsletter by [clicking here].

Summary Of the Markets Today:

The Dow closed down 29 points or 0.07%,

Nasdaq closed down 176 points or 0.90%,

S&P 500 closed down 25 points or 0.43%,

Gold $2,638 up $20.00 or 0.760%,

WTI crude oil settled at $72 up $0.08 or 1.13%,

10-year U.S. Treasury 4.573 up 0.028 points or 0.616%,

USD index $108.44 up $0.31 or 0.29%,

Bitcoin $93,551 down $636 or 0.68%, (24 Hours),

*Stock data, cryptocurrency, and commodity prices at the market closing

Today’s Highlights – Market Summary

US stocks experienced a decline on Tuesday, December 31, 2024, as they wrapped up a year characterized by significant gains. Despite this dip, the S&P 500 is up approximately 23.8% for the year, the NASDAQ is up nearly 30%, and the Dow has gained around 13%. The year was marked by a strong performance driven largely by advancements in artificial intelligence and the so-called “Magnificent Seven” tech stocks. This rally occurred alongside a notable shift in monetary policy, with the Federal Reserve implementing its first interest rate cut in four years and investor optimism surrounding President-elect Donald Trump’s return to office. In commodities, gold has risen over 27% this year, marking its largest annual gain since 2010, while Bitcoin has surged over 100%, although it recently retreated from earlier highs. However, recent trading sessions have shown a slowdown, contrasting with the typical “Santa Claus” rally that often occurs at year-end.

Today’s Economic Releases Compiled by Steven Hansen, Publisher:

The S&P CoreLogic Case-Shiller U.S. National Home Price 20-City Composite posted a year-over-year increase of 4.2% in October 2024, dropping from a 4.6% increase in the previous month. Home price growth continues to moderate across the U.S. Brian D. Luke, CFA at S&P CoreLogic Case-Shiller perspective:

Our National Index hit its 17th consecutive all-time high, and only two markets – Tampa and Cleveland – fell during the past month. The annual returns continue to post positive inflation-adjusted returns but are falling well short of the annualized gains experienced this decade. Markets in Florida and Arizona are rising, but not keeping up with inflation, and are well off the over 10% gains annually from 2020 to present. This has allowed other markets to catch up. With the latest data covering the period prior to the election, our national index has shown continued improvement. Removing the political uncertainly risk has led to an equity market rally; it will be telling should the similar sentiment occur among homeowners.

Here is a summary of headlines we are reading today:

Gold Price Rally Set to Continue in 2025

The Factors That Will Drive Oil Prices in 2025

Red Sea Shipping Rebound Forecasted for Late 2025

Ukraine To Quadruple Gas Transport Fees After Russia Deal Expires

Europe Faces Coldest Winter Spell As Gas Supply Concerns Mount

U.S. Gasoline Prices Set for Lowest Annual Average Since 2021 Next Year

S&P 500 posts 23% gain for 2024 as stocks close slightly lower in final session of year

Silicon Valley’s turn of fortune: Intel has worst year ever, while Broadcom enjoys record gain

Nearly all of Puerto Rico is without power on New Year’s Eve

Grayscale’s Zach Pandl reveals how politics and the economy are driving bitcoin’s bull run

A New Year’s Resolution: Let’s Get The US Out Of The Censorship Business

Market Outlook For 2025: Stuck Between An Inflationary Rock And An Economic Hard Place

Instead of sipping Champagne on New Year’s Eve, it may be time to invest in it

Click on the “Read More” below to access these, other headlines, and the associated news summaries moving the markets today.

EconCurrents will be transitioning to Substack in 2025. This newsletter will be discontinued no later than 01 March 2025 . All newsletter subscribers need to sign up for the EconCurrents Substack’s Newsletter by [clicking here].

Summary Of the Markets Today:

The Dow closed down 418 points or 0.97%,

Nasdaq closed down 235 points or 1.19%,

S&P 500 closed down 64 points or 1.07%,

Gold $2,622 down $10.30 or 0.38%,

WTI crude oil settled at $71 up $0.53 or 0.76%,

10-year U.S. Treasury 4.539 down 0.08 points or 1.732%,

USD index $108.07 up $0.07 or 0.07%,

Bitcoin $93,991 up $340 or 0.36%,

*Stock data, cryptocurrency, and commodity prices at the market closing

Today’s Highlights – Market Summary

Stocks experienced a decline on Monday as the major indexes continued to struggle in the final week of 2024. This downturn followed a previous week marked by significant losses in major tech stocks, including Tesla and Nvidia, which contributed to a Friday decline of 1.5% for the NASDAQ and over 1% for the S&P 500. The anticipated “Santa Claus” rally, historically a positive period for the stock market, has not materialized this year. Since December 24, the S&P 500 is down nearly 1%, contrasting with its typical average gain of 1.3% during this timeframe since 1950. With only two trading days left in the year, investors remain hopeful for a rebound, as the S&P 500 has seen a substantial increase of over 25% throughout 2024, while the NASDAQ has risen more than 30%. In other news, trading on January 9 will be closed in honor of former President Jimmy Carter, who passed away at age 100. Despite current market challenges, analysts maintain that the underlying fundamentals supporting this year’s market gains remain intact, suggesting potential buying opportunities in early 2025.

Today’s Economic Releases Compiled by Steven Hansen, Publisher:

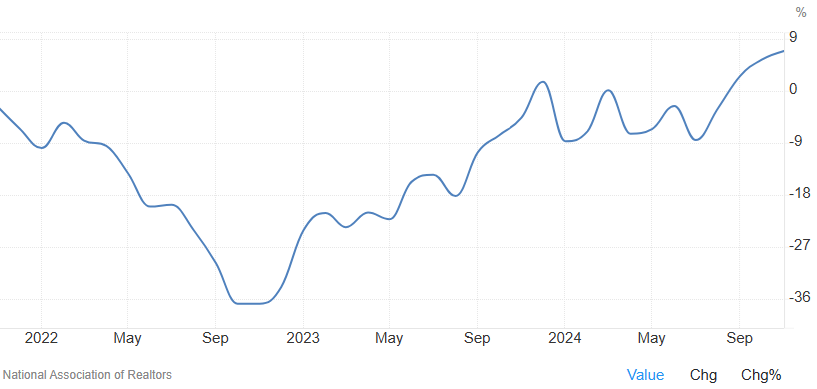

The Pending Home Sales Index (PHSI) grew 6.9% year-over-year. An index of 100 is equal to the level of contract activity in 2001. Will the growth in home sales be increasing? A year ago home sales where terrible – so growing year-over-year is not saying much.NAR Chief Economist Lawrence Yun added:

Consumers appeared to have recalibrated expectations regarding mortgage rates and are taking advantage of more available inventory. Mortgage rates have averaged above 6% for the past 24 months. Buyers are no longer waiting for or expecting mortgage rates to fall substantially. Furthermore, buyers are in a better position to negotiate as the market shifts away from a seller’s market.

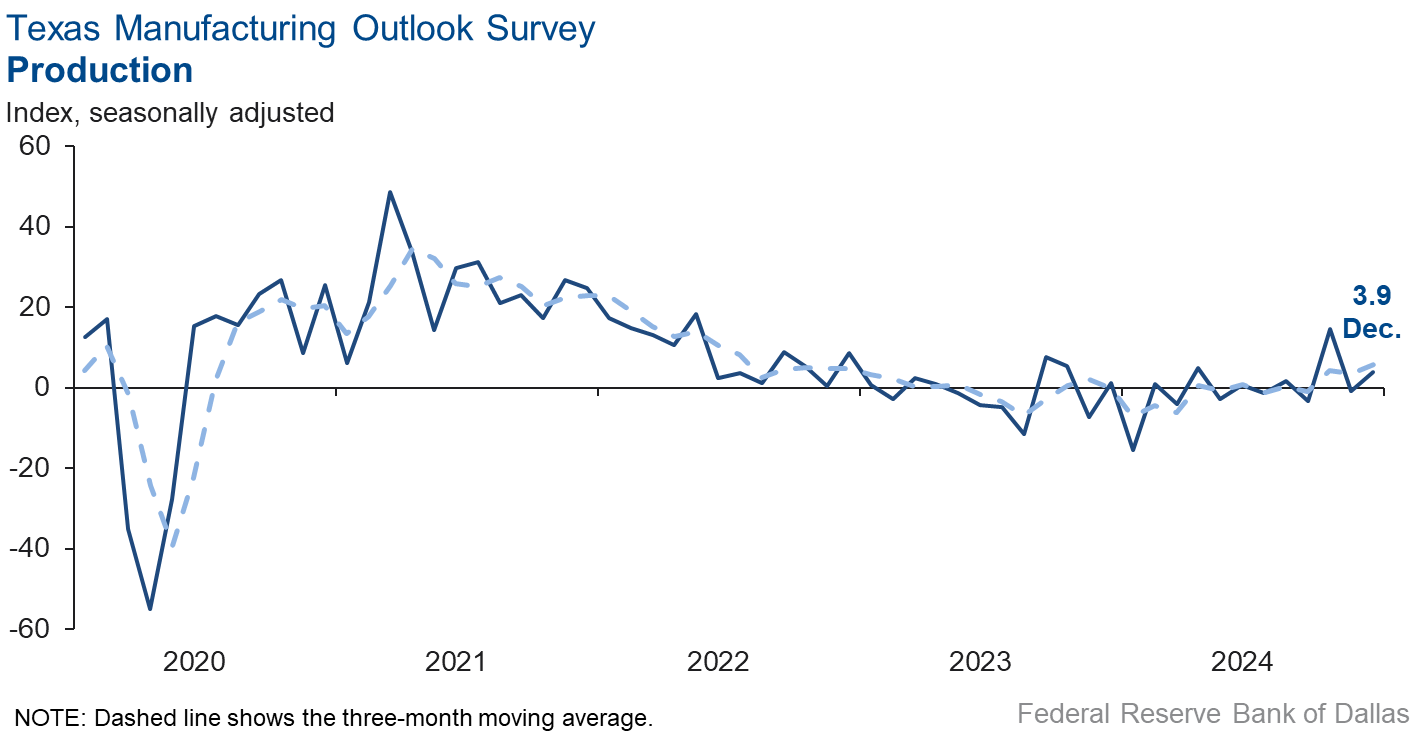

Dallas Fed Manufacturing activity increased in December with the production index rose to 3.9 from a near-zero reading last month. Other measures of manufacturing activity were mixed. The new orders index shot up 11 points to -0.9, suggesting demand was unchanged from November. The capacity utilization and shipments indexes both edged up but remained in negative territory, coming in at -2.5 and -2.0, respectively. Overall, this is a survey and based on opinion. Other regional surveys show contraction – and data shows manufacturing is in a recession in the U.S.

Here is a summary of headlines we are reading today:

Biden Administration’s Final Aid Package to Ukraine Aims to Bolster Defense

Carlos Slim Invested $1B In American Oil & Gas Companies In 2024

Ukraine To Quadruple Gas Transport Fees After Russia Deal Expires

Exxon and Chevron Expand Global Hiring Push

Europe Faces Coldest Winter Spell As Gas Supply Concerns Mount

U.S. Gasoline Prices Set for Lowest Annual Average Since 2021 Next Year

Turkey Says It’s Ready to Supply Electricity to Syria and Lebanon

Indian BPCL Boosts Middle East Oil Purchases as Russian Supply Dwindles

Oil Prices Flatline as 2024 Draws to a Close

Natural gas surges as much as 20% on expectations for colder-than-usual January on the East Coast

NYSE to close on Jan. 9 in honor of the late former President Jimmy Carter

Treasury yields dip as final trading week of 2024 kicks off

10-year U.S. Treasury 4.631 up 0.052 points or 1.136%,

USD index $108.02 down $0.11 or 0.01%,

Bitcoin $94,500 down $1,238 or 1.29%,

Baker Hughes Rig Count unchanged at 589 in the US – but the Canadian rig count fell from 166 to 96

*Stock data, cryptocurrency, and commodity prices at the market closing

Today’s Highlights – Market Summary

US stocks closed the holiday week with modest declines, capping off a largely successful year. The major indexes experienced slight pullbacks. Despite Friday’s negative session, the indexes maintained weekly gains: S&P 500: +1.8%, NASDAQ: +1.8%, and Dow: +1.5%. Notable tech stocks saw profit-taking: Tesla: -5%, Nvidia: -2%, and Amazon: -1%. The market is approaching the end of 2024 with an impressive annual performance: S&P 500 was up over 26% for the year, the NASDAQ Composite up more than 30%, and the Dow saw a modest rise of 14%. Investors focus on two key themes for 2025: the Federal Reserve’s interest rate strategy and the potential economic implications of Donald Trump’s return to the White House. The 10-year Treasury yield remained near seven-month highs at approximately 4.6%, signaling continued market volatility as the year concludes.

10-year U.S. Treasury 4.581 down 0.006 points or 0.087%,

USD index $108.12 down $0.08 or 0.07%,

Bitcoin $95,314 down $4,046 or 4.07%

*Stock data, cryptocurrency, and commodity prices at the market closing

Today’s Highlights – Market Summary

US stocks struggled to extend the Santa Claus rally today, with mixed performance across major indices. The S&P 500 and Nasdaq closed slightly lower, while the Dow Jones Industrial Average managed to eke out small gains. The Russell 2000, representing small-cap stocks, rose by 0.7%. The market struggled to build on the strong start of the Santa Claus rally, which began on December 24 with the S&P 500’s best Christmas Eve performance since 1974. Bitcoin (BTC) experienced volatility, falling to around $96,000. This decline affected crypto-linked stocks such as MicroStrategy. The Dow Jones Industrial Average has gained nearly 15% year-to-date. However, some individual stocks within the index have underperformed: Boeing (BA): Down 30% YTD. Nike (NKE) down 29% YTD. These performances contrast sharply with the overall positive trend of the index.

Today’s Economic Releases Compiled by Steven Hansen, Publisher:

In the week ending December 21, the advance figure for seasonally adjusted initial claims 4-week moving average was 226,500, an increase of 1,000 from the previous week’s unrevised average of 225,500. Unemployment levels are consistent with an expanding economy.

Here is a summary of headlines we are reading today:

Airports Around the World Are Going Green

Power of Siberia Hits Full Throttle

India’s Oil Demand Growth Set to Surpass China’s

Russia’s LPG Prices Fall 50% Following EU Embargo

Finland Boards Russian Shadow Fleet Tanker After Subsea Cables Go Offline

Rio Tinto’s Billion-Dollar Lithium Bet

India Adds 4GW of New Coal Power Capacity in 2024

China’s EV Uptake Is Years Ahead of Targets and Forecasts

China Plans the World’s Biggest Hydropower Dam in Tibet

36% of Americans took on holiday debt this year — averaging $1,181 — survey finds. These tips can help

Waymo dominated U.S. robotaxi market in 2024, but Tesla and Amazon’s Zoox loom

More than 90% of 401(k) plans now offer Roth contributions – but only 21% of workers take advantage

End Of Road: EV Startup Canoo Puts Employees On “Mandatory Unpaid Break”

President-Elect Trump Posts Christmas Message To “Wonderful Soldiers of China”, “Governor Trudeau”, And Greenland

Putin Reveals Biden Offered To Postpone Ukraine’s NATO Entry As Compromise

Click on the “Read More” below to access these, other headlines, and the associated news summaries moving the markets today.